A "Better" Guide to Estate Plan Funding, Part 5: A Revocable Trust Alone Is Not Enough

What documents should accompany a revocable trust?

This is Part 5 of the series on funding the estate plan. For the first part of this series and a series index, click here.

NOTE: I have made this article and video generally available to all readers and subscribers. That being said, this material is not intended to serve as attorney marketing and is created for the education of other wealth transfer professionals. If you are an individual in need of assistance, please contact a qualified professional and do not rely on this material as legal or tax advice. Also, while most of the material is behind a paywall, please do not subscribe to access the material if you are an individual in need of assistance.

Table of Contents

Intro

In the last video and article in this series, we explored some foundational myths and issues with revocable trusts themselves. This series is building towards strategies on funding the revocable trust, balanced with identification of other beneficiaries for nonprobate assets.

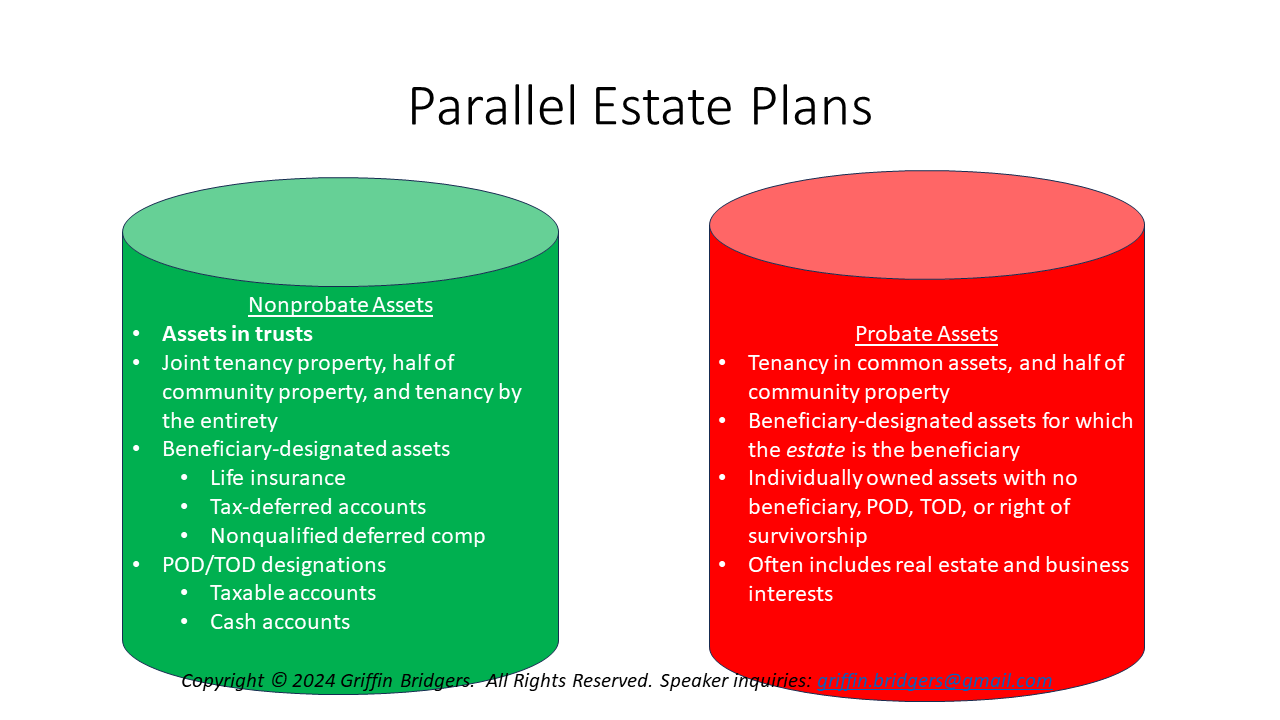

As a refresher, modern estate planning now involves two parallel estate plans. Each can be thought of as a bucket of assets. The nonprobate bucket is considered first, because by operation of law these types of transfers are given priority. They often pass directly to individuals by way of a right of survivorship, beneficiary designation, or POD/TOD designation, and thus bypass the terms of estate planning documents (but sometimes subject to claims of creditors). Wills, and even intestacy statutes, usually apply to probate assets unless there is a failure of beneficiaries, a disclaimer, or the estate itself becomes beneficiary.

Another key complication between these two parallel plans involves the processes for making changes to the estate plan. A change to the probate bucket involves updating a will, and while there are formalities needed to do so, the change will apply to all assets in the probate bucket. Contrast this to changes to the nonprobate bucket, which often requires changes to be made to each individual asset.

Is it possible to update the individual assets of the nonprobate bucket once, such that subsequent changes can be made in one document? Possibly. We previously explored the use of testamentary trusts under a will, compared to revocable trusts. Testamentary trusts are reliant on the valid execution of a will - which may not always happen (with no prejudice to either attorney-drafted documents or documents generated online) - with the added complication that some banks and custodians may not accept a beneficiary designation for a trust that does not yet exist.

This gives a nod to the revocable trust, which tends to be the target of polarizing opinions. Many of the reasons used to justify the use of a revocable trust are not absolute - such as probate avoidance, privacy, and ease of administration - but are often marketed as absolutes in a way that is designed to cast doubt on the expertise of those who do not recommend them. Nonetheless, the revocable trust is often easier to execute and update. The problem comes in how the trust is identified - a source of common errors.

The errors do not stop in proper identification of the trust, however. Both probate and nonprobate assets have to be manually transferred into the trust, either during life or through a transfer effective at death. To effectively do so, we must consider fiduciary authority to finish the job if we don’t. That is the substance of today’s discussion.

Video

Slides

Key Takeaways

As noted above, a revocable trust has to be funded - often on an asset-by-asset basis during life. What happens, however, if we never get around to funding the trust?

Since the trust usually contains the terms for the disposition of our assets at death, we run the risk that these terms may not legally apply to certain assets not transferred to the trust during life. We have already discussed the fact that nonprobate assets pass directly to named beneficiaries, and if these beneficiaries are not the revocable trust itself, then its terms will not apply to these specific assets. However, what about probate assets? Without taking into account the revocable trust, they are subject to the terms of a will or intestacy statutes if not placed into the trust. (Note that once assets are in the trust, they can no longer be considered probate or nonprobate assets).

To avoid probate assets passing outside of the revocable trust, we need a specific type of will called a pourover will. The will should contain a catch-all disposition, called a residuary clause, and the unique feature of a pourover will is that the revocable trust is identified as the sole beneficiary under the residuary clause. In effect, the will “pours over” any probate assets titled in our individual name into our revocable trust at death so that these assets can also be disposed of according to the terms we have thoughtfully included in our revocable trust.

Obviously, the assets disposed of under the pourover will are subject to probate unless there is a small estate exception that applies (which may require personal property and real property to be under a certain dollar amount, and may not be available if there is a valid will to begin with). But, without the pourover will, there would be intestacy - a much worse outcome.

The pourover will appoints an executor or personal representative (interchangeable terms depending on the state) to transfer probate property to the revocable trust, after respecting certain reporting and notice requirements under the probate process. At that point, the (successor) trustee of the revocable trust takes over. And while these roles can be filled by the same person, they are separate fiduciary roles with separate authority that may not fully cross over. In other words, while a revocable trust can give some of the executor’s authority to the trustee, it cannot appoint the executor - only a will can (which usually requires signature by a competent testator in the presence of at least two disinterested witnesses).

Another risk is the ability to fund the revocable trust if we become disabled or incapacitated. In the absence of legal planning, a court may appoint a conservator or guardian of property (again, interchangeable terms) to manage our individually-owned assets - which can be burdensome, as discussed with beneficiary designations of minors. Assets of the revocable trust at the time of disability or incapacity often escape the reporting and jurisdiction of the court and appointed conservator, and can be used privately for our care during a period of disability or incapacity. But, how can assets get into the trust after we become disabled or incapacitated?

This is where a durable power of attorney comes into play. This document names an agent or attorney-in-fact (interchangeable terms) to help manage our individually-owned assets. However, the general authority granted to an agent under many general durable powers of attorney - whether form documents or under state law - may not include the power to transfer our assets to a revocable trust. So, either having a custom-drafted clause granting the agent this authority, or a stand-alone durable power of attorney granting this authority, is a helpful backstop to this contingency which may also ease the burden of conservatorship.

In this vein, consideration needs to be given to whether the agent’s authority is immediate, or whether it is “springing” (i.e., only effective upon certification of incapacity by a court or one or more physicians). While an individual may prefer for an agent’s general authority to be springing, immediately-effective authority for an agent to transfer assets to a revocable trust can be helpful.

The extent of the agent’s funding authority, however, can affect this decision. For example, powers of an agent to change beneficiary designations to the revocable trust, or to take trust-level actions (like amending the trust, or removing and replacing trustees) are subject to abuse and as a result may be considered “hot powers” that have to be expressly listed and consented to (often by initials) in a durable power of attorney. These types of authority may be better suited for “springing” effectiveness.

With both documents, a common error is misidentification of the trust. Under the common-law doctrine of incorporation by reference, the revocable trust agreement can be referenced as part of a will or durable power of attorney. While now relaxed in some states and situations, this common-law doctrine usually requires the revocable trust agreement to exist at the time of incorporation by reference - meaning the trust should technically be signed before the pourover will and durable power of attorney are executed.

The trust must also be adequately identified - usually by name and by date of original creation. Simply stating “my revocable trust” is generally not specific enough to adequately identify the trust. While the incorporation by reference doctrine does not prohibit incorporation of future amendments to the revocable trust, it is also important to expressly incorporate any future amendments or restatements. Again, this is the type of language that may not always be found in form documents or online documents.

Conclusion

Coming up next in this series, we will explore another divisive topic - whether spouses or partners should use individual revocable trusts, or a joint revocable trust. We will later get into specific strategies for titling assets in the trust (as opposed to individual titling), along with nuances applicable to beneficiary designations.

Again, I need to remind you that this is not complete guidance and should not be relied upon as such. Unique client and family circumstances, such as blended families and complex business holdings/buy-sell agreements, may necessitate different types of planning considerations. That being said, if you are a wealth transfer professional who wants to continue to learn more about this topic of funding the estate plan, please subscribe and follow along. If you are not ready to take the plunge on a paid subscription, this course and article series will be available for purchase when completed.