A Gameplan for the Corporate Transparency Act

A course for attorneys, law firm owners, business advisors, and compliance professionals

Preview, and How to Contribute

To preface, I went back and forth as to whether to make this an exclusively-paid course. Given the importance of the subject matter, I opted for a hybrid “freemium” model as I will explain below - mainly as an experiment for future paid course offerings.

Either way, this will at least serve as a preview of what my new “paid” offerings will look like. Starting in 2024, I will offer paid courses, supplemented by video and separate written materials. My goal is to give you 3-4 courses a year, along with more exclusive office hours and encore Q&A sessions to supplement the courses. In terms of what is on tap, you can expect courses on grantor trusts, the post-SECURE Act regulations on RMDs (when finalized), C and S corporations for estate planners, gift and GST tax reporting for various trusts and strategies, and portability returns.

For now, instead of making this a paid course, I am turning to you to determine how much value it adds for you. My original sticker for this course was $249, and you are certainly capable of listening for free - especially because I do not have this course approved for CLE credit. But, if you want to kick my suggested price back to me, or at least go through the course and contribute what you think it is worth to you, click here to submit a payment. And, if you want to claim self-study credit where available, the materials should give you enough info to do so.

Again, click here if you would like to support this course.

The Course

This article serves as the roadmap for my new course on the Corporate Transparency Act. To learn more about the course, listen to this video (corresponds to slides 3-5 in the materials linked below):

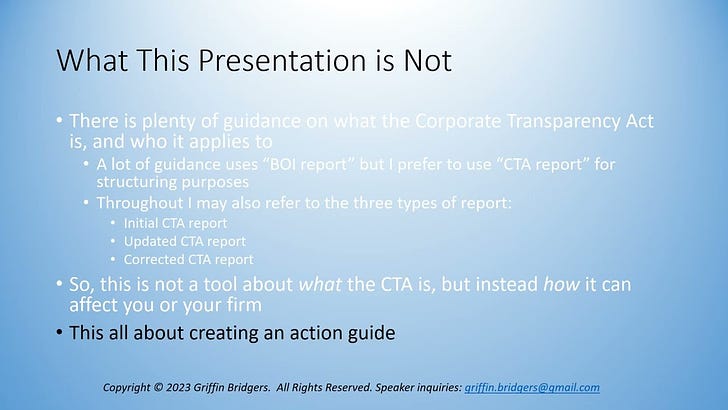

To start, this is not designed to be a full primer on what the Corporate Transparency Act (the “CTA”) is, or how it affects businesses. There are tons of explanatory materials out there already. Instead, the purpose of this course is to allow you to make a game plan for serving clients who have needs relating to the CTA while also recognizing some of the ethical and business risks that accompany CTA-related services.

However, I use a lot of terms that are unique to the CTA while assuming you know those terms. So, if you are starting fresh, I would encourage you to listen to this guide:

Written Materials

Here are the materials I put together to supplement this course. I have put these first so that, if you want to claim self-study credit, you are able to represent that you had access to the course materials. The materials include:

Course slides

An internal checklist on implementing the CTA for you or your firm/organization

A sample written mailer for clients

Sample language to be used in forms (do not use this without independent review and editing- this is provided for informational purposes only)

The Course

Once you have listened to the intro, videos 2-11 are included chronologically below along with the slides to which each video corresponds (numbered to include title slide and bio slide as slides 1 and 2).

Video 2 (Slides 6 - 9)

This video covers some of the broader expectations - both for this course, and the expectations between you and your clients with respect to the CTA. This video sets up the central goals of determining what services you will provide, notifying clients in either a specific or general matter, and most importantly cutting off any express or implied expectation a client might have that you will be handling the filing of a CTA report.

Video 3 (Slides 10 - 13)

In this video, we shift our focus internally to your firm or organization. If you will assist with creating entities on or after January 1, 2024 that may be treated as reporting companies, then filers within your organization will likely be treated as company applicants for CTA purposes. This video focuses on some of the basic concerns about identifying and limiting the scope of company applicants.

Video 4 (Slides 14 - 17)

This video continues the internal focus, this time on items such as conflict checks and the defining of services. A central question and starting point is whether to assist with the filing of CTA reports. In this vein, it helps to be clear to clients about which of the three types of report - initial, updated, or corrected - you may assist with. It also helps to consider whether, for example, certain types of transactions or documents could result in a change in beneficial ownership and thus an updated CTA report.

Video 5 (Slides 18 - 21)

In this video, some of the data gathering and privacy issues inherent in assisting with the CTA are presented - especially the storage and retention of information of individuals or entities you do not represent.

Video 6 (Slides 22 - 26)

This video first addresses changes to engagement letters which might be relevant to the CTA, along with perhaps the radical idea of adding to your e-mail signature some level of CTA disclaimer (much like we used to see with IRS Circular 230).

From there, we shift course to cover FinCEN identifiers and concerns relating to updated CTA reports. Finally we tee up an intro to some other services which can be provided outside of the filing of CTA reports.

Video 7 (Slides 27 - 30)

After determining what services you will and will not provide, notifying clients is paramount. In this video, we further discuss some of the ethical tensions between notifying some but not all clients, while also protecting yourself from any breach of unspoken expectations that could arise from not specifically notifying clients. This is all part of a broader strategy of getting info out about the CTA, whether by general or specific notice.

Tweaks to disengagement letters, or even use of CTA-specific disengagement letters, may be important as discussed.

Video 8 (Slides 31 - 33)

This video provides a hodgepodge of info to shift gears into non-reporting assistance. Outsourced compliance (and related data security concerns) along with determining beneficial owners are just two of a handful of related services discussed. This video also tees up the challenges of identifying beneficial owners where multiple classes of ownership are involved, which we expand on in the next video.

Video 9 (Slides 34 - 37)

Indirect beneficial ownership creates an extraordinary challenge to be navigated by reporting companies and their advisors. In this video we introduce the concept of “look-through analysis” where one entity owns an interest in a reporting company, and some of the related math. We also discuss some issues around the edges with determining equity ownership, such as where convertible debt, buy-sell agreements, purchase options, and even series LLCs might be involved.

Video 10 (Slides 38 - 42)

Beyond simply determining equity ownership, the concept of substantial control can throw a snag in the beneficial ownership analysis. In this video, we discuss substantial control, where it might pop up by accident (especially for updated reports), and wrap up by examining entity exemptions. All of these constitute analyses you could provide, but if you agree to assist with CTA reports, you may obligate yourself to also provide these analyses.

Video 11 (Slides 43 - 47)

This is the concluding video, containing my closing remarks and a summary of some of the key points from this series.

Course Conclusion

I hope this information proves valuable for you and your organization. Again, if you wish to make a non-refundable contribution towards this course, please click here. Or, if you prefer to contribute in other ways, the best things you can do are (1) share this course with your firm, or network (including on LinkedIn), and (2) subscribe to my newsletter to get first dibs at office hours and future courses (paid and unpaid).

Also, please note that this course is not complete. Part of the reason I used this format is because updates will be needed, and creating a dynamic course that is responsive to your needs is important to me. So, if you have any questions or changes, please reach out.