On September 13, 2021, news of tax proposals from the House Ways and Means Committee threw the planning world into a tizzy. For a time, we had to confront the possibility of significant changes to grantor trusts, which generated polarizing views (primarily with respect to chances of actually being enacted as law).

October 28, 2021 may have brought some clarity, as the most recent proposed text of the Build Back Better Act from the House Rules Committee eliminated two of the most problematic proposals - a change to the taxation of grantor trusts, and a reduction of the basic exclusion amount. But, as is often the case, there are a number of practitioners claiming that the grantor trust proposal is not dead - yet.

Either way, all we can do is plan for what is put in front of us on a day-to-day basis. Which is why I have put together the following video summary of the pared-down proposals applicable to trusts and estates:

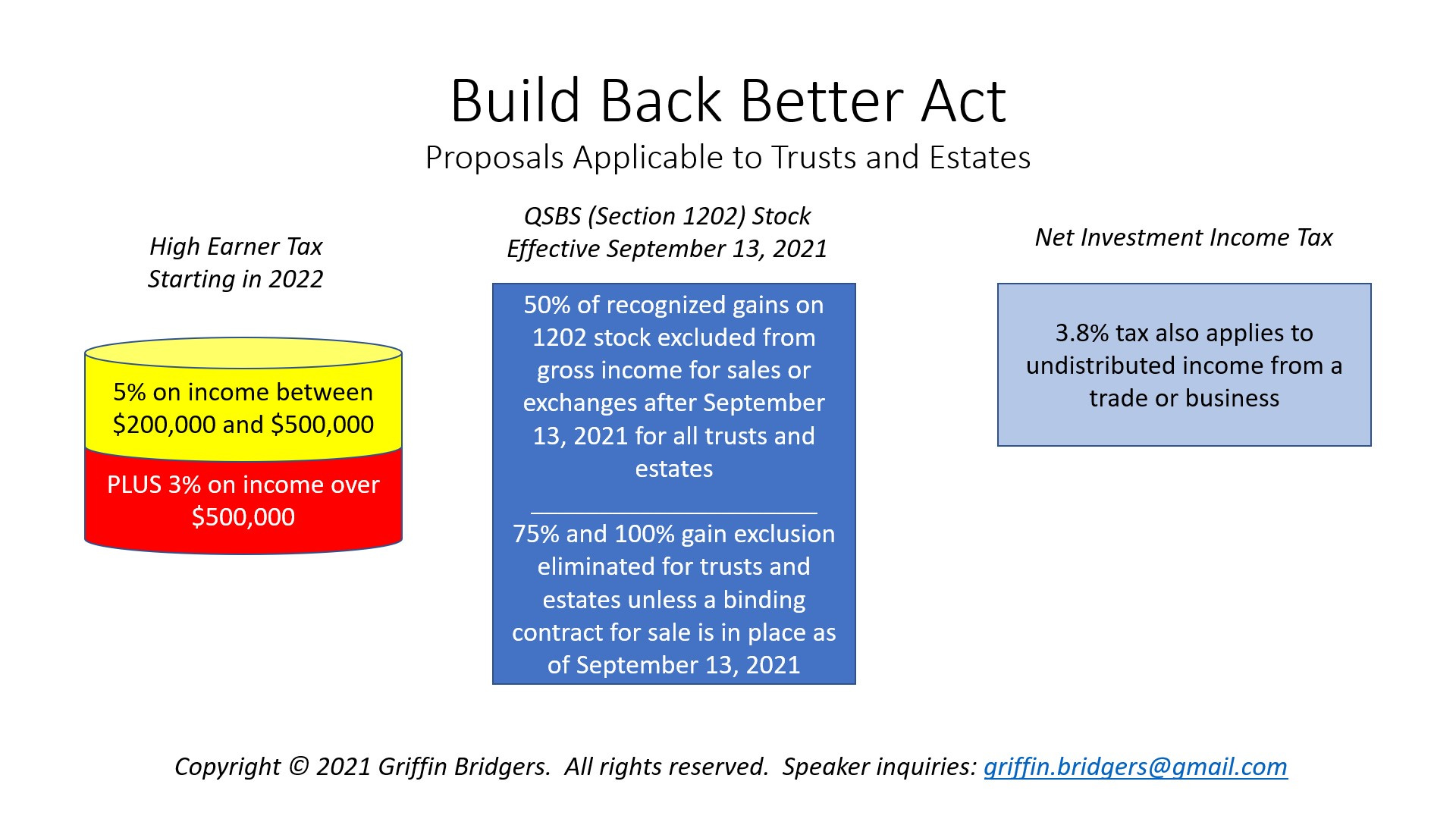

If you do not like watching or listening to videos, the following are the key changes to know about:

Undistributed income of an estate or nongrantor trust could be subject to a high earner tax of 5% on amounts over $200,000, plus an additional 3% on amounts over $500,000;

The 100% gain exclusion for the first $10,000,000 of gains on the sale of qualified small business stock (QSBS) under IRC Section 1202 may be eliminated and replaced with the default 50% gain exclusion for sales or exchanges not subject to a binding contract as of September 13, 2021 (but no change has been proposed to the possibility of stacking multiple QSBS 50% exclusions through multiple nongrantor trusts); and

The net investment income tax (NIIT) of 3.8% could be expanded to include trade or business income not distributed by an estate or nongrantor trust, which (in addition to the high earner tax) could increase the federal income tax on estates and nongrantor trusts by up to 11.8% per year.

And, in case you would like a visual summary, I have extracted the following slide from the video above:

For now, your guess is as good as mine as to the finality of these proposals. For the time being, however, all you can do is plan for the element of surprise - with only 60 days left in 2021, we will continue to have less and less time to react to those proposals (if any) which may survive the gauntlet of the House and Senate. For the time being, optics appear to control over function, and this most recent set of proposals could be nothing more than a smokescreen to avoid the appearance that talks have stalled.