Griff's Notes, February 8, 2022: It's Gift Tax Return Season - Here is a Cautionary GST Tax Tale

Tax, trusts and estates updates from around the country

Recently, there have been some good private letter rulings highlighting the issue of allocating GST exemption where an estate tax inclusion period (ETIP) is involved. I spoke about one such ruling - PLR 202148003 - in a recent video, although my analysis was incomplete (for reasons I will highlight in this article):

Yet another private letter ruling was published on February 4, 2022 - PLR 202205019 - which also deals with this issue.

As many of you know, it is gift tax season (in addition to income tax season), meaning that law firms and tax preparers nationwide are gearing up to report the many gifts that occurred in 2021 (presumably motivated by a desire to use gift and GST tax exclusions in the face of threatened tax reform which did not occur).

But, for those clients who prepared trusts which have a contingency of being included in their gross estate if they fail to outline the trust term (such as a GRAT or a QPRT), these types of trusts have an issue with respect to the GST tax exemption. While I will not get granular in terms of the Code citations (as this narrative can be better traced in the PLR linked above), I think it is helpful to outline the rules for allocation of GST exemption in this scenario.

As a starting point, any transfer to a trust that has GST potential (i.e., a born or unborn skip person is a current or remainder beneficiary) which occurs after December 31, 2000 is eligible for the automatic allocation of GST exemption so long as it meets the definition of a “GST trust” (which we will not get into in great detail). Of course, you can also manually allocate GST exemption (in full or in part) on a transfer tax return if you first elect out of automatic allocation. This is an important exercise on Part 2, Schedule D of the gift tax return (Form 709) as reflected in the following image:

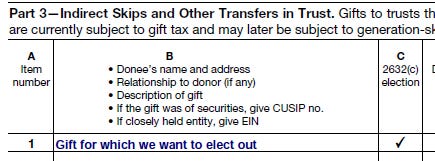

As you can see, lines 5 and 6 allow for this two-step process - election out of automatic allocation of the GST exemption on Line 5 (by attaching an election out statement), followed by a manual allocation (by attaching a notice of allocation) on Line 6. But, to get to this point, you also have to check the box on Column C of Schedule A to elect out of automatic allocation as seen in this image:

This procedure is designed to apply if GST exemption is allocated concurrent with the completion of a gift for the calendar year or tax year in question. But, some transfers are not eligible for either automatic allocation, or manual allocation, at the time of transfer - those which involve an ETIP with respect to the transferor or the transferor’s spouse. In other words, if the grantor or the grantor’s spouse were to die immediately after the transfer, would the transferred assets be included in their gross estate? If the answer is yes, and if there is a 5% or greater actuarial chance that the grantor or grantor’s spouse would not outlive the ETIP, you cannot allocate GST exemption at the time the transfer occurs.

A lot of practitioners misinterpret this scenario to mean that no GST exemption needs to be allocated, and accordingly that no election out statement needs to be filed. This is, however, incorrect.

There is a little-known procedure that may necessitate another gift tax return at the close of the ETIP (if the ETIP closes during the life of the transferor or transferor’s spouse). Why? Because the ETIP simply defers the allocation of GST exemption until the ETIP closes. And, at the time that the ETIP closes, GST exemption will be automatically allocated based on the FMV of the transfer at that time if there was no prior election out.

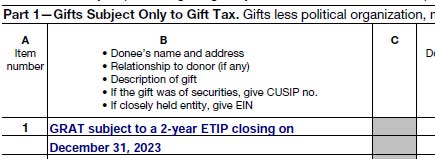

Now, you can forego this procedure by electing out of the automatic allocation of GST exemption at the time an ETIP transfer occurs (or any time prior to the close of the ETIP) pursuant to IRC Section 2632(c)(4). But, doing so requires reporting the ETIP transfer in the correct part of Schedule A. Many practitioners assume that the ETIP should be reported on Part I, Schedule A, by assuming that the ETIP is not subject to GST tax. But, this may prevent you from electing out. As seen below, the box to elect out on Column C of Part I, Schedule A is greyed-out:

And, if you did not previously elect out of automatic allocation of the GST exemption when the ETIP transfer was funded by either misrepeporting the ETIP, or simply not completing Schedule D or an election-out statement, you need a gift tax return to elect out at the close of the ETIP. Without doing so, the GST exemption may be wasted.

To best illustrate this, we will consider a GRAT. The attractiveness of the GRAT is that the combination of a retained annuity which qualifies under IRC Section 2702, and a term which may end before the death of the grantor, allows for the subtraction of the present value of the annuity from the value of the property transferred to the GRAT. When done right, a GRAT with a high enough annuity and low enough term can have a little or no gift tax value.

So, a GRAT uses little or no gift tax applicable credit. It would stand to reason, then, that the GRAT would also use little or no GST tax exemption. But, as noted above, the GRAT usually creates an ETIP, so no GST tax exemption can be applied to the gift. So, you cannot create a GST-exempt transfer from the outset. This wouldn’t make sense anyway, because you would not want to waste GST exemption on the present value of an annuity interest that would come back to you during the GRAT term.

It may be possible, however, that a GRAT does not create an ETIP if its term is short enough relative to the age of the grantor or the grantor’s spouse. If the actuarial chance of the grantor dying during the GRAT term is less than 5%, there may not be an ETIP. But, this still does not relieve you of the need for an election-out statement. The GST allocation in such a case may not be based on the present value of the remainder interest, but instead on the FMV of the property transferred to the GRAT.

So, the solution is simple. When funding the GRAT, or any ETIP transfer for that matter, it should be reported as an indirect skip on Part 3, Schedule A if there is any GST potential with respect to the current or remainder beneficiaries. The image of this part, and the corresponding box to check to elect out of automatic allocation, was included above. (Of course, you should also include an election-out statement).

Now, if you come across a gift tax return where there is an ETIP and no prior election out, all is not lost. There is still time to elect out, up until the due date for a gift tax return for any transfers occurring in a calendar year in which the ETIP closes.

In fact, the instructions for Form 709 contemplate this exact result. There is a procedure for filing a 709 solely due to the close of an ETIP, found on Page 4 of the 2021 Instructions for Form 709:

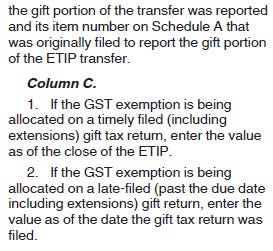

Starting with the end in mind, this means that you will at least have a pared-down gift tax return (according to these instructions) in the year the ETIP closes. There is also an obligation to complete Part I, Schedule D (image further below) according to the following instructions:

But, there are also explicit instructions for ETIPs on Part 1, Schedule D of the Form 709. As noted in the following instructions, we must clearly identify gifts which create an ETIP, by including this in the description of the gift in Column B.

Conclusion

Gift tax returns can be tricky, especially for those practitioners who are not well-versed in GST tax. But, by following the right procedures, you can avoid the need for a private letter ruling down the road. Because, after all, this was the result in the PLRs cited above - a taxpayer had relied on a tax preparer who failed to advise on the election-out procedure where an ETIP was involved, and by the time it was discovered it was too late. In other words, it was discovered after the filing deadline for the gift tax return with respect to the year in which the ETIP closed.

Luckily, in the case of these PLRs, the IRS found reasonable reliance on a tax professional - this is your ticket to entry - and allowed for a late election-out statement. But, there is still a significant user fee, along with the fees to have a tax professional prepare the request for determination. All of this could have been avoided if there had simply been either an election out of automatic allocation when the ETIP transfer was funded, or at the close of the ETIP period. It is rare to get two bites at the apple to correct an issue such as this.

So, the key takeaway is to review your clients’ gift tax returns for ETIPs that may close in this or a later year. If you find one, check to see if there was an initial election out of automatic allocation. If not, make a point to file a gift tax return for the year of the close of the ETIP to avoid automatic allocation at that time.