Non-Grantor Irrevocable Complex Discretionary Spendthrift Trusts: A New TikTok Darling

Run for the hills if this strategy is proposed to you

While TikTok, in its current iteration, does not fit with my method of providing information or even my target audience, it can still create headaches for us as tax professionals. While many of the ideas promulgated on TikTok have some gray areas, one fairly recent idea does not.

The central idea is that the taxable income of an irrevocable non-grantor trust can be zeroed out on IRS Form 1041. How? By using a misreading of IRC Section 643 to treat trust (taxable) income as an “extraordinary dividend” that is exempted from the definition of “income” under IRC Section 643(b). As a result, it is claimed that income tax can be avoided by shifting income-producing assets to such a trust.

This strategy, sometimes colloquially known as the “irrevocable non-grantor complex discretionary spendthrift trust” (as if we did not already have enough lengthy trust names) has been making the rounds of the TikTok sphere. Its proponents (none of whom I will give free promotion to) do not appear to be attorneys or CPAs, but instead those who are trying to shill information products for real estate investment.

This is also on the radar of the IRS - recently a Chief Council Advice Memorandum was issued regarding the promotion of the strategy. It has a great analysis of why the reasoning is wrong, but I thought I would provide my own with a bit more color than the IRS has the liberty to provide.

In some sense, I get odd satisfaction in tearing down these proposals, which otherwise should not be given the time and attention I dedicate below. But, I thought it might help you as a tax or wealth transfer professional to get a sense of why this does not work, in case a client approaches you with a question we all dread: “My advisor proposed this to me. Can you help?”

Mechanics

At the trust level, the strategy simply appears to be an offshoot of a trustee’s authority to allocate between income and principal. Where the rubber meets the road, and where the risk appears, is in the reporting of trust income on IRS Form 1041.

Luckily, one purveyor of this strategy was so kind as to recently illustrate the exact reporting mechanics on the 1041 on a TikTok video. I took the liberty of capturing some screenshots, which admittedly are not as clear as they could be due to the scaling of size from the actual video.

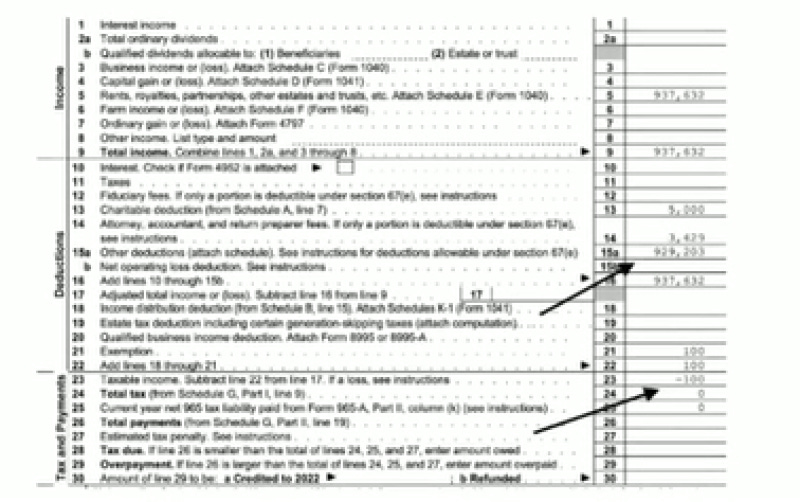

As seen in this first screenshot, we have a trust with income of $937,632:

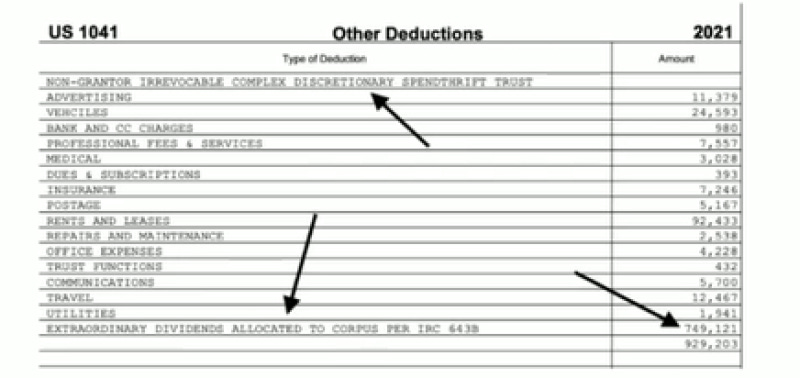

Next, a screenshot is provided of a schedule of “other deductions,” noting that a net sum (after subtracting other possibly legitimate economic deductions) of $749,121 is being “deducted” as “extraordinary dividends allocated to corpus per IRC 643(b).” This creates total “other deductions” of $929,203.

This deduction is then carried over to Line 15a of the 1041, to support a net loss of $100:

So, if you are at all familiar with Subchapter J of the Internal Revenue Code, you may see the flaw in reasoning here. In case you don’t, I will walk you through an analysis that is much longer than it needs to be, yet not as comprehensive as I could have made it.

Income Exclusion Theory

IRC Section 643(b) does not define “taxable income” for all purposes of Subchapter J. Instead, if you want that definition, you need to go back to IRC Section 641(b), which provides that a trust’s “taxable income” is computed in the same manner as for an individual, except as otherwise provided elsewhere in Subchapter J. This is further refined in Treas. Reg. 1.641(a)-2, providing that “gross income” of a trust is determined in the same manner as for an individual, and Treas. Reg. 1-641(b)-1, allowing the same deductions to a trust as for an individual other than the deductions described in IRC Sections 651 and 661.

If we go to IRC Sections 651 and 661, we find deductions for amounts distributed or required to be distributed to a beneficiary during the tax year. Without diving into the details and mechanics thereof, I will note that this deduction is capped by a yet-undefined term called “distributable net income.”

Where is the definition of this term, you ask? If you guessed IRC Section 643, you are correct. It is also in Section 643(b) that, as I mentioned above, we find the definition for the term “income.” The second sentence of this Code Section contains an exclusion from the term “income” and upon which the TikTokkers appear to be reading in isolation:

Items of gross income constituting extraordinary dividends or taxable stock dividends which the fiduciary, acting in good faith, determines to be allocable to corpus under the terms of the governing instrument and applicable local law shall not be considered income.

So, where is the disconnect?

For one, this exception has its own exception found in the first sentence of 643(b), which expressly states that the exclusion from the definition of “income” in that Code Section shall not apply when preceded by certain terms, which (for emphasis on my part) includes “taxable” and “gross.”

What does this mean in plain English?

The TikTok argument is that the exclusion of extraordinary dividends allocated to corpus from the bare definition of “income,” read in isolation, means that extraordinary dividends cannot be taxed as income to the trust.

The application of the first sentence of 643(b) means that the second sentence cannot be read in isolation - extraordinary dividends allocated to corpus, although not included in the definition of “income,” cannot be excluded from the definition of “taxable income” or “gross income” because the cited exclusion from the definition of “income” in the second sentence expressly does not extend to the definitions of “taxable income” or “gross income.”

A bit of a legal lesson - this concept is called esjusdem generis. Simply put, it means that in a statute or clause with multiple sentences, you cannot read later sentences in isolation if there are more particular preceding sentences.

Since IRC Section 641 expressly imposes the tax under Section 1(e) (the individual income tax) to the “taxable income” of trusts, extraordinary dividends allocated to corpus have to be taxed to the trust.

Now, if you are truly splitting hairs, I want to dive a bit deeper here. The TikTokkers are inconsistently making two separate and disparate arguments, even if they do not know it. One, they are essentially arguing for an exclusion from gross income. Two, they are arguing for a deduction of extraordinary dividends allocated to corpus. But, these are two separate things - items of income are either excluded from gross income, or deducted, but they cannot be both. Why? Because taxable income is gross income net of deductions. Something can only be excluded from the definition of taxable income by virtue of being allowed as a deduction. Exclusion from the definition of gross income means the excluded income cannot also be a deduction.

Continuing on our analysis, I want to again note that 643(b)’s exclusion to the exclusion does not exempt extraordinary dividends allocated to corpus from the definition of “gross income,” either. In fact, the first four words of the second sentence expressly state that the sentence applies to items of gross income to begin with! Since Treas. Reg. 1.641(a)-2 expressly states that “gross income” of a trust is determined in the same manner as for an individual, without exception, there can be no gross income exclusion under a trust that is not also granted to an individual. These exclusions are exclusively (pun intended) found in IRC Sections 101-140. Nowhere in these Code Sections do we find any reference to dividends, much less extraordinary dividends. In fact, the only deduction relating to dividends - IRC 243 - only applies to corporations, and not individuals or trusts.

Nonetheless, the 1041 sample above attempts to shoehorn this supposed “gross income exclusion” into the Form by treating it as a deduction (which, as I noted, its an item of tax significance that is separate and independent from exclusions). If this were truly an item excluded from gross income, it would not be reported as gross income on Form 1041 to begin with.

Nonetheless, there is one item that ties these two concepts together, which just so happens to explain the context of the misinterpreted definition above. That concept?

Expenses.

Expenses of the trust may be tax-deductible, but in order to be tax-deductible, they can’t just be paid from income. Instead, they must be paid from - you guessed it - gross income.

Now, when we dig into the economics of our trust, we might find that some actual (accounting) income was, indeed, excluded from gross income under the rules applicable to individuals under IRC Sections 101-140. What if, then, we use this excluded income to pay some or all of our expenses? This means we cannot deduct the portion of expenses actually paid from this income that is excluded from gross income.

It is in this vein that we find part of Form 1041 relating to this (“Other Information,” Page 3, Line 1) - upon which we report tax-exempt income and “exempt-interest dividends” with a provisio to also attach a computation of the allocation of expenses.

So where am I going with this?

If anywhere, it is on this line that the trust would have an obligation to report extraordinary dividends allocated to corpus if they were indeed excluded from income, along with a report of what expenses were actually paid from such purported dividends. (But, they are not tax-exempt interest.)

So, by reporting the extraordinary divided allocated to corpus in the income section to begin with, and then as a deduction, without in any way, shape, or form representing how it can be tax-exempt income on the appropriate sections of Form 1041, the TikTokkers are completely failing to report the income in a manner that is consistent with “their” interpretation of IRC Section 643(b).

And speaking of this interpretation, what truly is the context of the term “income” in this scenario? Why exclude extraordinary dividends allocated to corpus from this definition to begin with?

Deduction Theory

To address that, I am going to generously give credit and assume that the TikTok interpretation of 643(b) intended to claim that it is, indeed, a deduction by virtue of exclusion from “taxable income.” After all, we concluded above that it cannot be excluded from “gross income,” not just simply due to the fact that the cited sentence expressly applies to items of gross income but also due to the fact that the same exclusions from gross income apply to both individuals and trusts under a plain reading of IRC Section 641 and its Treasury Regulations. But to get there, I need to look at some specific definitions.

Now, what I am not going to spend much time on is the definition of “extraordinary dividend” - admittedly I can do more research but (for reasons I will set forth below) I don’t need to.

Let’s start with dividends. Paraphrasing the plain meaning, dividends are distributions to equity holders of a business entity from currently-taxed or previously-taxed earnings on business capital. So, whether the trustee can indeed by alchemy declare that any item of income is a “dividend” much less an “extraordinary dividend” seems far-fetched - after all, why include that specific term in the statute if the trustee has such broad powers? The term itself needs to mean something, doesn’t it?

Within the Tax Code, the only definition of “extraordinary dividends” appears to be in IRC Section 1059(c), which defines an extraordinary dividend as a dividend which exceeds 10% of a shareholder’s basis in common stock in a C corp or 5% of a shareholder’s basis in preferred stock in a C corp. Outside of the Tax Code, the only relevance of the term “extraordinary dividend” appears to be in the context of insurance companies and affiliated groups relating thereto.

So, the chances of all forms of trust income being treated as “extraordinary dividends” is suspect, at best. While it is rare to have C corp stock held by a trust, it is possible that there could be dividends meeting this definition (which have their own tax rules under 1059). But, with a pass-through entity, the trust’s distributive share of income cannot be classified as a dividend at the tax level because the trust is taxed on its share of entity income, regardless of whether or not the income is distributed in cash as a dividend (ordinary or extraordinary) to the trust.

Further, 643(b) does not refer to a trustee’s power to declare that something is an extraordinary dividend - it simply refers to a trustee’s power to allocate the extraordinary dividend to corpus. At the end of the day, it is this trustee action that leads to the supposed tax “loophole” whereby the extraordinary dividend is allocated to corpus.

Not to mention, the power is not absolute under 643(b) - there is a requirement that a trustee’s allocation of extraordinary dividends to corpus not be made in “bad faith.” I don’t know about you, but notwithstanding the refrain of Judge Learned Hand ("Anyone may so arrange his affairs that his taxes shall be as low as possible; he is not bound to choose that pattern which will best pay the Treasury, there is not even a patriotic duty to increase one's taxes…"), I do not find the actions of a trustee who is forcing all income to take on a contrived definition and be allocated to corpus solely for purposes of carrying out a contrived reading of the Tax Code to be in good faith.

In other words, there is no way for a trustee to observe the loophole’s good-faith requirement while claiming the benefit of the loophole itself.

So, we have these two phantom terms - “income” and “extraordinary dividends” - that shouldn’t have us tied in knots but somehow do anyway because of some random non-attorney talking heads trying to sell house-flipping classes some 15 years after Armando Montelongo first popularized that income stream (which, ironically, he is now being sued for by his students based on fraud and racketeering). But, I digress.

That brings us back to the question of deductions, which is where our definition of “income” comes in. Now, what I have not yet cited, and what the TikTokkers conveniently do not cite, are the Treasury Regulations - particularly Treas. Reg. 1.643(b)-2 - which add color to this supposed “exclusion.” Not only do we see our “bad faith” exception to the exception to the exception repeated, but we now see some specific citations as to where such items come into play - in the computation of “distributable net income.”

Distributable Net Income - Setting Up for the Knockout

This brings us full circle back to the one deduction cited earlier that individuals cannot claim, but trusts can, under Treas. Reg. 1.641(b)-1.

So, the second sentence of Treas. Reg. 1.643(b)-2 essentially gives us a roadmap of exactly where we need to look for context of how extraordinary dividends allocated to corpus (instead of income, as I will later explain) come into play. In the grand scheme of things, the only areas in which we see income (as an unqualified term) have any context is in the source of money flowing out of the trust - expenses (as previously mentioned), and distributions.

Which brings us to a mismatch which I previously alluded to with expenses. There is a mismatch between accounting income, and taxable income, for purposes of a trust. Taxable income is gross income net of deductions, in either case excluding the types of income that are not treated as gross income to an individual as thoroughly established above. Both expenses and distributions may be paid out of accounting income, but they can only be deducted from gross income to the extent paid out of gross income.

(And, in the case of pass-through entities owned by the trust, the trust could even have phantom income attributable to its pass-through entity ownership. In this case, there is no accounting income until after-tax dividends are paid to the trust as I alluded to previously, but there is gross income.)

Accounting income really represents the physical income generated in cash by another component of the trust - its corpus, also (more commonly) known as its principal. Corpus represents the previously-taxed assets held by the trust. But, from a traditional accounting perspective, income generated by corpus includes portfolio income - dividends, rents, royalties, etc. Capital gains are usually not treated as income, but instead as corpus.

Without getting into the storied history, Subchapter J gives deference to state law powers granted to trustees to make the judgment call as to what forms of cash windfall, especially capital gains, are treated as income or corpus. Why does this matter? Because trusts often have income and remainder beneficiaries. A trustee has to balance the needs of both income and remainder beneficiaries, which means there is a tension between the two when it comes to investment of trust corpus. Investments in income-producing assets may benefit the income beneficiaries at the expense of remainder beneficiaries. On the other hand, since capital gains are allocated to corpus, investment in appreciating assets (which do not generate as much current income) may benefit the remainder beneficiaries at the expense of current income beneficiaries.

To make sure that the tax results match with this economic reality of fiduciary duties, Subchapter J recognizes that the tax liability should correlate to the trustee’s (good faith) decisions. So, “income” that is distributed is generally taxed to beneficiaries that receive it. However, “income” that is retained is taxed to the trust. And, capital gains that are allocated to corpus are taxed to the trust, whether distributed or accumulated, unless the trustee exercises a power under state law or the trust instrument to allocate capital gains to income instead of principal or unless the trust requires capital gains to be currently distributed. In either such case, capital gains would be taxed to a beneficiary.

More clearly put, the only context of the term “income” taken in isolation is not determining what income is taxable to begin with - it is determining who is taxed on the income. No matter what, either the trust or the beneficiary is going to be taxed on each and every item of income that is not excluded from gross income, or deducted. So, if something is excluded from the term “income” taken in isolation, it simply means that it cannot be taxed to the beneficiary. Instead, it means that “income” has to be taxed to the trust, regardless of whether or not that item is distributed.

To track this at the trust level, trusts have all income (not specifically excluded from gross income) included in the trust’s initial income tax base. Then, there is a corresponding deduction for income actually distributed to beneficiaries during the trust’s tax year (usually a calendar year), or within 65 days of the end of the trust’s tax year (if the trustee elects to treat it as being distributed during the prior year).

This deduction is capped, however, at a certain amount - the “distributable net income” of the trust. This is all taxable income not allocated to corpus, plus tax-exempt interest (net of expenses paid from such interest), but not other items excluded from gross income.

Which brings us full circle - extraordinary dividends in this context may be allocated to income or corpus by a trustee, and the latter case is what the supposed “loophole” in IRC Section 643(b) is referring to. But, looking further at this context, the only consequence of such an election by the trustee is to shift the taxation of extraordinary dividends that are actually distributed to beneficiaries, or to retain tax liability within the trust by allocating such dividends to corpus. And, in the case of a trust that is required to distribute all income, the trust can only be taxed on extraordinary dividends if they are both allocated to corpus, and retained in the trust. (The latter would not be the case for the “discretionary” trust being promoted on TikTok.)

All of this is a roundabout way of saying that there is no way extraordinary dividends can be deducted unless they are actually (1) used to pay a trust expense, or (2) actually distributed to an individual beneficiary or charity (which has its own set of requirements under IRC 642). If there is no deduction, there is no way to exclude extraordinary dividends from the taxable income of the trust. And if there is a deduction, that is simply shifting the taxation of income actually paid in cash from the trust - there cannot be a deduction for income kept in the trust, period.

The Knockout Punch

Even if somehow all of this works, it is completely contingent on the trust being taxed as a complex, non-grantor trust. Notwithstanding the fact that I routinely see mistakes in trusts and trust forms that inadvertently create grantor trusts, there is one fatal flaw to this strategy:

To achieve the desired outcome, the grantor can never benefit from the trust.

Now, some of the TikTokkers are smart enough to note that the grantor should not take any distributions of the supposed tax-free income out of the trust. But, they propose something even more stupid - taking loans from the trust.

Anyone familiar with IRC Section 675(3) knows that while any loan to the grantor is outstanding, the trust may be treated as a grantor trust. The only way to avoid this is to (1) provide for adequate interest and security in the loan terms, and (2) have an independent trustee (who is not related or subordinate to the grantor) make the loan. Finding an independent trustee willing to go along with the scheme is easier said than done. Further, a simple promissory note usually does not address the requirement of adequate security.

Even worse, I’ve yet to see a TikTokker advocate that loans from the trust must bear adequate interest, and that the grantor must put up security for the loan. Unless the grantor has sufficient assets in their own name, their ability to provide adequate security is suspect. Use of trust assets to secure the loan won’t work. Further, the grantor is probably leveraged to the hilt in these situations being peddled by real estate investment “gurus,” and may already have pledged personal assets for real estate investments by the trust itself. How likely are those lenders to respect the grantor’s (likely subordinate) pledge of assets to take a cash loan out of the trust?

Conclusion

I have spent more time dissecting this issue than needed. And, I know that this article is not going to convince any promoter of the strategy that they are wrong - in fact, if any of them who reads this will probably come up with some other twisted interpretation of the Tax Code or some other ad hominem attack against me. What I hope to do is convince you - the practitioner - to run for the hills if a client, or promoter, attempts to rope you in to the preparation of such a trust and/or the preparation of Form 1041 for such a trust.

And, of course, if you are an individual considering this strategy, I would also encourage you to run - not for the hills, but to your legal and/or tax advisor because this article is written for educational purposes only and is not intended to substitute for legal or tax advice.