This is a continuation of the series on everything you ever wanted to know about estate planning trusts. For an intro and index to this series, please click here. The linked article will have a series index that gets updated periodically as well, so please bookmark it.

Table of Contents

Intro

To understand the credit shelter trust, it helps to understand the common trust division outcomes which occur at a decedent’s death. For this discussion, we will focus primarily on married couples. While a trust created at the death of an unmarried individual could technically be a “credit shelter trust,” such a label may only be appropriate when the estate tax liability is zeroed out by use of the estate tax charitable deduction.

In this vein, a credit shelter trust is funded with a finite amount - an amount sufficient to zero out estate tax taking into account the available estate tax applicable credit. For this reason, it is best deployed in the presence of a companion trust which qualifies for the the estate tax marital deduction and/or the estate tax charitable deduction. The name of the trust derives from this outcome - that it shelters the decedent’s remaining, unused applicable credit.

Alternative Names

Credit shelter trusts are usually created at death. When reviewing an estate plan, it is rare that the name “credit shelter trust” is actually used, however. More often, you will see a term like the “family trust,” “bypass trust,” or “B trust.”

The term bypass trust gives us a hint at the estate tax treatment of the trust. Often, as we will explore below, a surviving spouse is a primary beneficiary of the credit shelter trust. If the deceased spouse has children and descendants, they may also be beneficiaries of that trust. Then, when the surviving spouse dies, children and descendants become primary beneficiaries through a variety of options we will later discuss. But, the assets of the credit shelter trust are not included in the surviving spouse’s gross estate for federal estate tax purposes (assuming the trust was structured correctly). In other words, the assets “bypass” the survivor’s gross estate.

In an age of high exclusions, this bypass feature is often not as great of a concern. In fact, there is a tax trade-off in the form of a basis step-up for appreciated credit shelter assets at the death of the surviving spouse if these assets are included in the survivor’s gross estate. But, this basis step-up is highly inefficient. Why? Because it means that both spouses’ estate tax exclusions (and GST tax exemptions) were applied to the same assets or same trust twice. We will discuss the GST tax issues further below.

Structure

This outcome is perhaps the most important feature to keep in mind when it comes to reviewing and analyzing the structure of a credit shelter trust. While a surviving spouse can have a power of appointment over the credit shelter trust, care must be taken to avoid structuring it as a general power of appointment.

It is important to note, however, that a general power of appointment may not be express but instead implied. For example, if a spouse is a trustee of the credit shelter trust, the spouse’s distribution powers to themselves should be limited to an ascertainable standard such as health, education, maintenance and support - otherwise a general power of appointment could be created. Further, if children and descendants who are dependents are also beneficiaries of the trust, the spouse should be expressly disqualified (as trustee) from exercising any distribution power in a manner that could discharge any legal obligation the spouse may have to support such beneficiaries.

In a blended family, spousal powers of appointment may not be a good idea. This could apply even if later remarriage creates a blended family. So, if a spousal power of appointment is included, the appointees should be sufficiently limited to avoid disinheritance of the remainder beneficiaries of the first spouse to die. For this reason, powers of appointment often define appointees from the perspective of the descendants of the deceased spouse, instead of the descendants of both spouses. Further, while charities could be appointees, the appointment of principal may not be efficient (due to the fact that credit shelter trust assets are already exempt from further estate tax). On the other hand, a lifetime power to appoint income to charity could be beneficiary.

When we consider testamentary versus lifetime powers of appointment, care must be taken to avoid creation of lifetime powers that lead to gross estate inclusion with respect to the surviving spouse. But, lifetime limited powers of appointment could create flexibility so long as the appointees are sufficiently limited to address the concerns from the prior paragraph.

On occasion, credit shelter trusts may grant a spouse a five by five power, which is the right (on an annual basis) to withdraw the greater of $5,000, or 5% of the trust assets by value. By limiting the withdrawal power to this $5,000/5% limitation, the spouse avoids making a gift to the other trust beneficiaries if and when this power lapses at the end of each calendar year (if not earlier). There may be some adverse GST tax consequences, however, to this power of withdrawal which we will later discuss. So, this type of power will usually be used in a share of a credit shelter trust that is not exempt from GST tax.

In line with these gift tax concerns, spousal powers of appointment can also become problematic where a disclaimer is involved. If the spouse exercises a power to disclaim any direct transfers, or transfers to a marital trust, then certain requirements must be met in order for the disclaimer to be a “qualified” disclaimer. The tax significance of a qualified disclaimer is that the spouse making the disclaimer will never be treated as the gift, estate, or GST tax owner of the trust assets. In order to accomplish this outcome, the spouse cannot be given any power of appointment (general or limited) over the disclaimed assets. For this reason, a credit shelter trust funded with disclaimed assets is sometimes treated as a separate trust called a “disclaimer trust.”

The significance here is that a spouse disclaiming into a credit shelter trust must also disclaim any power of appointment over the credit shelter trust, if the power of appointment is not sufficiently limited to avoid application to the disclaimed assets. But, there are a couple of special carve-outs. One, a spousal trustee’s distribution powers by themselves should not disqualify the disclaimer so long as they are limited to an ascertainable standard, as noted in Treas. Reg. 25.2518-2(e)(2). Two, if a spouse has a five by five withdrawal power over the credit shelter trust, this power does not need to be disclaimed as noted in Treas. Reg. 25.2518-2(e)(5), Example (7).

Of course, there could be a savings feature for a spousal power of appointment over disclaimed assets if the disclaimer is not qualified. Why? If a spouse makes a disqualified disclaimer, they become the new gift tax owner of the disclaimed assets. But, by retaining a testamentary (limited or general) power of appointment over the disclaimed assets, the surviving spouse avoids making a completed gift at the time of the transfer under Treas. Reg. 25.2511-2(b). This at least defers the inefficient outcome of using both spouses’ applicable exclusions on the same trusts. The trade-off, of course, is inclusion of the disclaimed assets in the surviving spouse’s gross estate (with accompanying basis step-up potential). It also avoids the application of IRC Section 2702 to the credit shelter trust.

Ironically, I often see spousal powers of appointment drafted in a way that limits application to disclaimed assets. But, if the power of appointment is just limited to assets for which there is a qualified disclaimer, perhaps that is a better outcome.

This spousal testamentary power of appointment can also be important in a joint revocable trust, if the surviving spouse’s contributions (intentionally or unintentionally) become irrevocable at the death of the first spouse. Again, this prevents a completed gift that would otherwise use the surviving spouse’s applicable exclusion at the time of disclaimer.

Funding Formulas

We will discuss funding formulas in another set of articles, because it is rare that the credit shelter trust will be funded immediately after the decedent’s death (even though it is funded using values as of the date of the decedent’s death). Assets may fluctuate in value between date of death and date of funding, and certain assets and income may be used for expenses of administering the estate and revocable trust. (With the right formula, however, there should be no estate tax and thus no estate tax apportionment because estate tax is often deferred until the surviving spouse’s death by transferring the remainder to a marital deduction trust.)

A credit shelter trust does not have to be exclusively created, or funded, at a decedent’s death. The first spouse to die is treated as the settlor of the credit shelter trust. But, lifetime transfers may also “shelter” the applicable credit of the first spouse to die through the use of a spousal lifetime access trust, or SLAT. In this vein, many of the tax principles that apply to a credit shelter trust also apply to a SLAT. On the other hand, a credit shelter trust will usually be taxed as a complex trust - the funding of the trust at the death of the settlor means the traditional grantor trust rules cannot apply unless the spousal beneficiary retains a power under IRC Section 678(a).

Importantly, though, the final value of a credit shelter trust may not be settled for a while. The amount to be transferred, while over-generalized, is limited to the remaining estate tax applicable exclusion. This amount is reduced by (1) lifetime gifts, (2) failed lifetime gifts pulled back into the gross estate which pass to others, and (3) any other transfers made at death which do not qualify for the estate tax marital or charitable deductions. These amounts could all be adjusted by the IRS as part of the review of a 706.

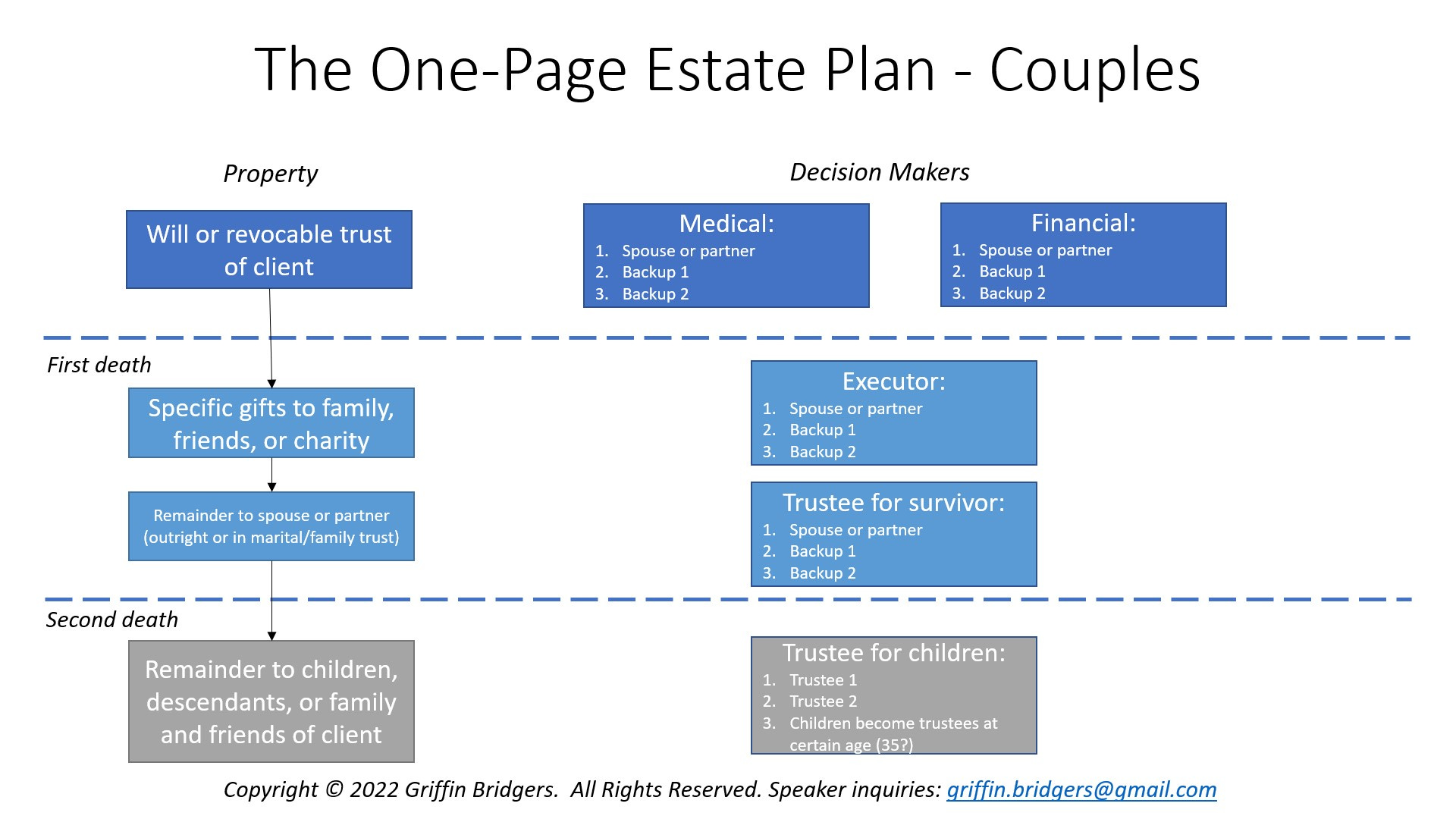

A good way to think of the credit shelter trust is an extension of the “sweetheart” estate plan between spouses. This plan usually just transfers all assets to a surviving spouse at first death, with the balance to children or descendants at second death. Of course, as illustrated below, the spousal gift at first death is first reduced by nonspousal gifts (which also use estate tax applicable exclusion if not transferred to a qualifying charity):

In this vein, the credit shelter trust (which is usually used in conjunction with a marital deduction trust) is simply a way to convert the spousal gift from an outright transfer into a transfer in trust. There are a variety of non-tax benefits to do so (such as protection of trust assets if a surviving spouse is sued, or remarries, along with earlier benefit to children and descendants without waiting until the survivor’s death), but this credit shelter structure traditionally guaranteed that the applicable exclusion of the first spouse to die would not be lost forever.

Direct spousal gifts (to a U.S. citizen spouse) automatically qualify for the estate tax marital deduction, thus resulting in a loss of the applicable exclusion of the first spouse to die, so use of a credit shelter trust within the traditional “sweetheart” distribution scheme limits this possibility to the extent the first spouse to die has sufficient assets to use the entire exclusion. (For a noncitizen spouse, transfers at death will use applicable exclusion unless passing to a qualified domestic trust, or QDOT).

With the advent of the portability election, this potential loss of exclusion has been limited. But, portability still requires the exercise of filing Form 706, and the value of assets passing to a credit shelter trust cannot be estimated. But, the lack of a credit shelter trust in an estate plan is no longer the catastrophe it once was from an estate tax perspective with the onset of portability. A variety of structures can now be used to “bypass” (pun intended) the rigidity of the traditional mandatory funding formula, including the traditional loss of a step-up in basis for credit shelter trust assets at second death.

These outcomes, however, cannot be examined in the vacuum of the remaining applicable exclusion. We must also consider the GST exemption, which is a use-it-or-lose-it exemption that is not preserved by the portability election.

GST Tax Issues

As discussed in a prior article, lifetime gifts (especially gifts subject to Crummey powers) can create a mismatch between the remaining applicable exclusion at death, and the remaining GST tax exemption. Where remaining GST exemption is less than remaining applicable exclusion, the outcome is a credit shelter trust that is not fully exempt from GST tax.

In this vein, funding formulas may allow optimal allocation of GST exemption to create one share of the credit shelter trust that has an inclusion ratio of zero (the GST-exempt share) and another share having an inclusion ratio of one (the GST-nonexempt share). Ideally, the exempt share should retain its zero inclusion ratio after the surviving spouse’s death, otherwise we end up also wasting both spouse’s GST exemption on the same trust.

Why is this a concern? One, if the surviving spouse has powers from the outset that could result in any portion of the credit shelter trust being included in the surviving spouse’s gross estate, this creates an estate tax inclusion period (ETIP) that could prevent any of the GST exemption of the first spouse to die from being allocated to the credit shelter trust or a share thereof. The outcome could be a permanent loss of this exemption. And, even if this prior allocation was allowed, any future inclusion in the gross estate of the surviving spouse causes the surviving spouse to become the new “transferor” of the included assets for GST tax purposes, which resets the prior inclusion ratio to one except to the extent the surviving spouse can allocate their own GST exemption to the included assets.

I alluded to issues with five by five powers above. If we dig into Treas. Reg. 26.2632-1(c)(2), we discover that avoiding the ETIP rule requires a less than a 5% probability that property will be included in the gross estate of the surviving spouse. We also discover that five by five powers do not create an ETIP, but this only occurs if the withdrawal right continues for no longer than 60 days. So, a spousal five by five power from principal should be structured to last no longer than 60 days, instead of the usual calendar year that is often considered. And, for optimal effect, limiting the five by five withdrawal power to the principal of the GST non-exempt share may be more efficient when we consider the possibility that up to 5% of this share could be included in the surviving spouse’s gross estate (with corresponding resetting of prior GST allocations) at the surviving spouse’s death.

All this being considered, if you remember nothing else, remember that any gross estate inclusion in the surviving spouse’s gross estate could significantly frustrate the GST tax outcomes of the credit shelter trust.

Conclusion

While there is much more we could discuss on credit shelter trusts, this should give you enough to address the high points from a drafting and review perspective. And, if it is discovered that there is an issue with a credit shelter trust during the surviving spouse’s life, there are often ways to fix it - perhaps not completely, but at least in a manner that creates more tax certainty.

The complexion of credit shelter trusts has changed significantly over time. Back when the applicable exclusion amount was only six figures, there were tons of credit shelter trusts created and funded primarily for asset appreciation - meaning there are lots of older credit shelter trusts with low-basis assets. But, in a high exclusion environment with possible sunset, emphasis has shifted to the lifetime funding of trusts such as SLATs that serve as the functional equivalent of credit shelter trusts. In fact, some estate plans simply pour over the remaining exclusion amount to an existing SLAT in lieu of creating and funding a new credit shelter trust.

In coming articles, we will explore trustees’ distribution powers in greater detail - especially against the backdrop of what is ideal for a trust such as a credit shelter trust. We will also explore marital deduction trusts, and the trusts created for descendants after the death of both spouses.