As a quick reminder, subscribers receive complimentary access to the Western Wealth Symposium - click here for more info. Respond to this e-mail to receive your promotional code. And, if you purchase a one-year paid subscription to this newsletter between now and December 11, you can also receive complimentary access.

Table of Contents

Intro

Leading up to the election, the planning zeitgeist has encouraged significant lifetime gift transfers to trusts for purposes of locking in part, or all, of our record-high estate and gift tax basic exclusion amount. This seems like a good idea on paper, but as discussed in prior content, the math does not work out unless you gift away more than the portion of the exclusion that might go away (often called the “bonus” exclusion). Even then, the benefit is only 40 cents for each dollar gifted over the bonus exclusion (based on a current maximum estate tax rate of 40%).

Now that we are facing Republican control of the Executive Branch, Senate, and (probably, but not certain as of the date of publication of this article) the House of Representatives, and without belaboring some of the nuances of requiring votes from Democrats under the Byrd Rule and/or budget reconciliation, we find a new unknown. There is now a greater possibility that the sunset of the basic exclusion amount may not occur. And while having perhaps a very low probability, we must also consider the possibility of wholesale repeal of the estate tax.

While prognostication is primarily an emotional and not a practical exercise at this point, it is certainly possible that we could face givers’ regret on a much broader scale than we saw after 2012 depending on Congressional action (or inaction) in the next 12-18 months. Which brings us back to the risks. If the sunset might not happen, how should we advise clients right now? Should we be focusing on the value in gifting outside of transfer tax savings, especially if one or more of our trifecta of federal transfer taxes (gift, estate, and generation-skipping) goes away?

If we focus on the income tax side of things, perhaps the greatest risk(s) relates to the income tax basis of transferred assets. In this article and follow-up articles to come, we go back to basics to discuss some of the rules relating to income tax basis for transfers during life (as opposed to transfers at death). Why? Because perhaps the biggest trade-off for lifetime gifts is the loss of a step-up in basis.

This article focuses on some of the general basis rules applying to gift transfers. Subsequent articles will explore nuances for the unified basis rule, grantor and nongrantor trusts, charities, net gifts, and split-interests, along with rules relating to depreciation of basis by the donee of property.

Basic Basis Rule for Appreciated Property

Generally, gifted assets are subject to what is known as a carryover, or transferred, basis rule under IRC Section 1015(a). In other words, a gift usually results in no change to basis for appreciated property.

There are, however, a few exceptions of note (not necessarily covered in this order within this article):

1. A part gift, part sale;

2. A gift of property with suspended losses under the passive activity loss rules;

3. A gift of loss property;

4. A gift where gift tax, or GST tax, is paid in conjunction with the gift; and

5. Interspousal gifts.

This carryover basis rule seems fairly basic in its operation and conclusion. But, there are some important nuances beyond carryover basis. Let’s take, for example, a gift of stock that has been held for 8 months by the donor. The donor bought the stock for $10 per share, and it was worth $100 per share at the time of the gift. Five months later, the stock has gone on a huge bull run and is now worth $250 per share – at which time the donee elects to sell it.

The donee’s basis in the stock will be $10 per share, and the donee will recognize gain of $240 per share. But, what is the character of such gain? Generally, a long-term capital gain requires an asset to be held longer than 1 year under IRC Section 1222(3). And, it would appear at first glance that our donee only held the stock for 5 months before sale – which generally would make this a short-term capital gain due to a holding period of less than 1 year. However, IRC Section 1223(2) allows a new owner to tack on their holding period to that of the prior owner when there was a carryover basis from the change in ownership.

What does this mean? It means the donee’s holding period of 5 months actually gets added to the donor’s 8 month holding period, giving the donee a deemed holding period of 13 months – which satisfies the 1-year threshold for long-term capital gains (generally resulting in preferential income tax rates under IRC Section 1(h)).

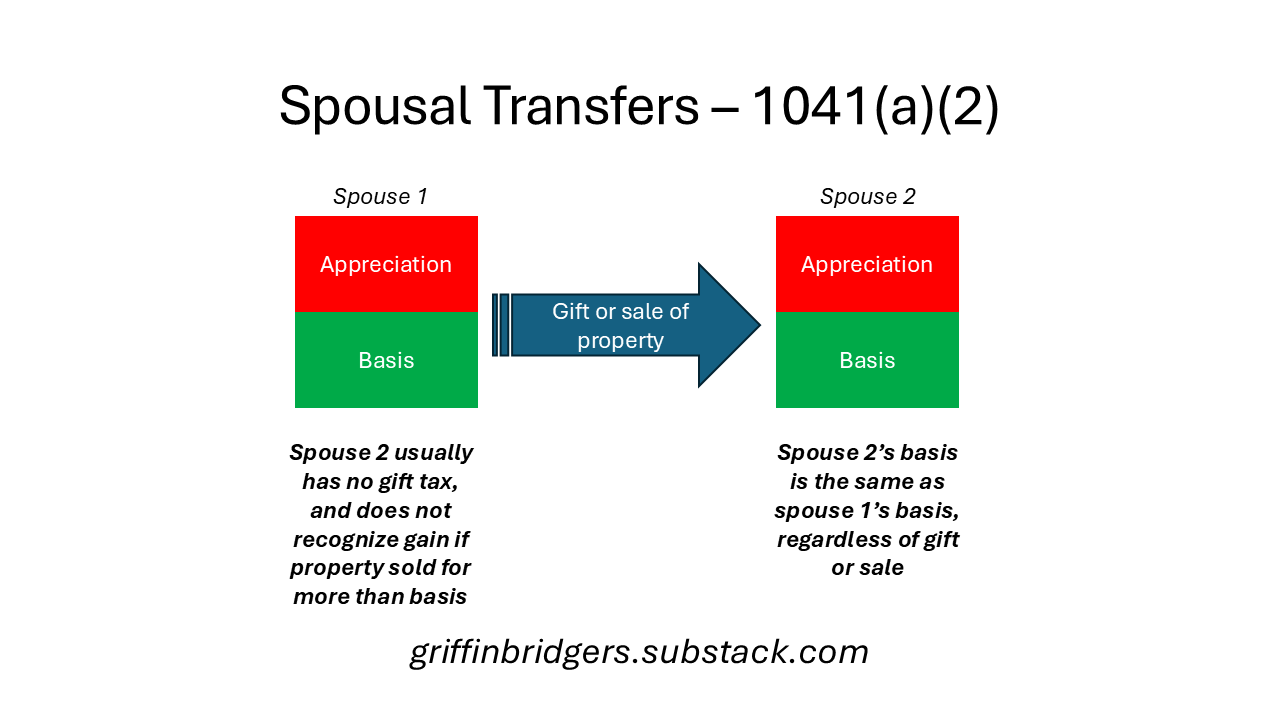

Note, however, that the carryover basis rule is different for any transfer to a current spouse, or to a former spouse incident to divorce, under IRC Section 1041(b)(2). IRC Section 1015(d) expressly provides that the rules of IRC Section 1041(b)(2) override when it comes to transfers between spouses. We will discuss the implications of this rule when there is a sale or exchange below, but for now please note that this generally creates a blanket carryover basis rule. It also creates an exception to the rules regarding basis of loss property with respect to a donee, to later be discussed.

Part Sale, Part Gift, and Transfers Between Spouses

Basis is irrelevant to gift tax, because it only applies for income tax purposes. Instead, gift tax only applies to the fair market value of the property transferred under IRC Section 2512(a) - whether lesser than or greater than the donor’s basis. For appreciated property, this means both basis and appreciation are subject to gift tax. But, for property with a value lower than its basis, this means the gift tax only applies to the (lower) fair market value – leading to an interesting outcome we will later discuss.

Importantly, however, IRC Section 2512(b) goes on to state that a transfer of property for less than full and adequate consideration results in a gift to the extent that the value of the property transferred exceeds the value of the consideration received in return. This is important to note for both transferor and transferee, because it is often assumed that a taxable sale or exchange of property (even at a bargain) in a transaction where gain is recognized creates a new cost basis in the purchaser under IRC Section 1012(a).

Treas. Reg. 1.1015-4 clarifies the basis rules in this situation. Generally, the donee/purchaser’s basis will be the greater of:

1. The consideration paid by the donee/purchaser, or

2. The basis of the property in the hands of the donor/seller.

In this situation, if the consideration paid by the donee/purchaser is greater than the donor/seller’s basis, then the donor/seller will usually recognize gain. And, if the donee/purchaser is a related party and the property is depreciable, such gain may be taxed as ordinary income under IRC Section 1239.

Recall however that all transfers between spouses, or former spouses (if incident to divorce), are subject to blanket carryover basis rules under IRC Section 1041(b)(2). So, for example, if a purchasing spouse pays consideration that exceeds the selling spouse’s basis, the purchasing spouse would still receive the selling spouse’s carryover basis as if this were a gift transfer (even if gain would be recognized if the transfer was not between spouses). Note that this rule could rear its ugly head where grantor trusts having spousal deemed owners are involved.

Gift of Loss Property

As noted above, the gift tax applies to the fair market value of gifted property – without regard to the basis of the gifted property on the date of the gift. But, this could create an odd dynamic where the basis of the gifted property is higher than its gift tax value since the gift tax only applies to the lesser of those two amounts.

For example, let’s assume the donor gifted shares of stock that had a gift tax value of $10 per share, but an income tax basis of $100 per share. In such a situation, it may be preferable for the donor to instead sell the stock and recognize the loss of $90 per share. But, let’s assume for whatever reason (perhaps being over the $3,000 net deductible capital loss limit under IRC Section 1211(b)) the donor prefers to gift the stock. (Note that if the donee was a grantor trust, the donor could still benefit from any loss recognized by the trust notwithstanding the rules below).

While it appears on paper that the stock is worth $10 per share to the donee, it may actually be worth much more when we consider the donee’s (hypothetical) ability to sell the stock and recognize a tax loss of $90 per share. Arguably, if this was possible, the stock would be worth much more than $10 per share. However, this option is not possible. Under IRC Section 1015(a), if the fair market value of gifted property is less than the donor’s carryover basis, then the donee’s basis (for purposes of determining loss) will be the fair market value of the gifted asset on the date of gift instead of the carryover basis.

In other words, you cannot gift an existing tax loss to someone other than a spouse. Where spouses are concerned, however, IRC Section 1041(b)(2) would supersede the application of this loss rule under IRC Section 1015(d).

But, if the property recovers in value, we end up with some interesting possibilities as illustrated below. If the property is later sold for more that its fair market value but less than the donor’s carryover basis, the basis is deemed to be equal to the amount received – thus resulting in no gain or loss to the donee. And, if the property fully recovers in value and is sold for more than the donor’s carryover basis, the donee gets to use the carryover basis for purposes of determining gain on the sale.

So while we cannot gift a tax loss, we can make a tax-free gift of “potential” gain (in the form of recovered basis) up to the donor’s carryover basis. This is an understated, but highly valuable, tax benefit to consider for loss property that has a high likelihood of recovering in value. A use case might be gifts of publicly-traded securities during a recession, under which (1) the donor doesn’t use as much gift tax applicable credit due to depressed values and (2) the donor’s higher basis can be gifted tax-free to the donee to avoid gain recognition on potential future appreciation.

Note that this rule can have interesting outcomes where a part-sale, part-gift is involved. Let’s say the donee/purchaser pays less than the donor/seller’s basis. If the fair market value of the property being sold is greater than the consideration paid by the donee/purchaser, but less than the donor/seller’s basis, this would appear to (1) cause a loss to be realized by the donor/seller, subject to related party rules under IRC Section 267, and (2) cause the donee/purchaser to inherit the donor/seller’s higher basis under Treas. Reg. 1.1015-4(a)(2). But, the flush language of Treas. Reg. 1.1015-4(a) addresses this, by noting that the donee/purchaser’s basis for purposes of determining loss cannot be greater than the fair market value of the property.

Gift of Passive Activity

One of the most frustrating rules in the Internal Revenue Code, IRC Section 469, deals with the rules surrounding deductions of certain losses known as passive activity losses. (This rule also applies to passive activity credits, which we will not discuss here.) Generally, this rule does not allow a taxpayer (including an estate or trust) to deduct losses from one or more passive activities in the aggregate, i.e., activities in which the taxpayer does not materially participate for the year, against any income other than aggregate passive activity income. Any excess losses get carried over to each subsequent tax year under IRC Section 469(b), until either (1) sufficient income from passive activities exists to absorb the suspended losses, (2) the income from the property or interest generating the disallowed losses is no longer passive (subject to some nuances beyond the scope of this article), or (3) the taxpayer’s interest in the passive activity is disposed of (the gain on which is characterized as passive for this purpose).

In the case of a gift of property generating passive losses, there is an interesting rule under IRC Section 469(j)(6). In such a case, any suspended passive losses (for the year of gift or carried over from prior years) get added to the basis of the gifted property. These losses then become nondeductible in the hands of the donee, because they have been added to the basis.

We have an ordering rule here which takes special importance. In particular, IRC Section 469(j)(6)(A) provides that this basis increase takes place immediately before the gift. Thus, this increased basis would become the donor’s new basis, which would then be carried over to the donee under the rules of IRC Section 1015(a). Because of the operation of this pre-gift basis increase, the loss rule highlighted above is preserved – that if the increased basis is higher that the fair market value of the gifted property, it cannot be used by the donee for purposes of calculating a loss on the sale of the property. But, it does create the tax-free gift of the excess of the donor’s basis (increased by suspended passive activity losses) over fair market value that we saw with loss property.

Gift Tax Paid

Generally, under the operation of Treas. Reg. Sections 2505-1 and 2505-2, no gift tax is ever payable out of pocket by a U.S. citizen or resident until the entire applicable credit against gift tax is exhausted, starting first with any deceased spousal unused exclusion (DSUE) until exhausted and then using any basic exclusion amount until exhausted. With a lower probability of the basic exclusion amount being lowered (by sunset or legislative action) as introduced above, the possibility of lifetime payment of gift tax becomes even more remote. More than likely, such a situation would arise in a gift tax audit that determines a deficiency.

(As an aside, any generation-skipping transfer tax paid out of pocket increases the value of the gift under IRC Section 2515. But, IRC Section 2654(a)(1) contains a similar rule to the ones we will explore below for the effect of gift tax paid on basis. It is more likely that GST tax would be paid out of pocket, as this can be accomplished simply by electing out of automatic allocation of GST exemption for direct skips.)

That being said, a significant difference between the estate tax and the gift tax is the effect on basis. For property transferred at death, basis is generally adjusted to the value of the property as finally determined for federal estate tax purposes under IRC Section 1014, with some exceptions. For gifted property, the carryover basis rule (subject to the exceptions above) creates our starting point. However, gifts and inheritances generally are excluded from gross income under IRC Section 102 because the estate and gift taxes reflect a shift of the burden of taxation to the transferor (or transferor’s estate).

For this reason, if gift tax is paid without a corresponding adjustment to basis, this would create an indirect income tax on the donee on appreciation that was also subject to gift tax (since the gift tax applies to the fair market value of property – including both basis and appreciation).

Since a donee would recover basis tax-free in a sale or exchange of property in a recognition transaction, there is no double-tax for the gift tax attributable to the basis in property. And, as we discussed above, it may even be possible to gift some bonus basis without payment of gift tax for this purpose if the fair market value of gifted property is lower than the donor’s basis. But, for the portion of any unrealized appreciation in gifted property that is attributable to gift tax, this could lead to a double-tax.

To remedy this outcome, IRC Section 1015(d)(6) provides for a basis increase (not above fair market value) for the portion of the gift tax attributable to net appreciation in the gift. As further clarified for post-1976 gifts in Treas. Reg. 1.1015-5(c), the determination of how much gift tax is attributable to net appreciation is based on comparisons between (1) the amount of the gift (net of deductions and annual exclusions, if any), (2) the net appreciation in the gifted property, and (3) the gift tax paid for all gifts during the year. This basis increase applies not just to a straight gift, but also a part-gift part-sale (see Treas. Reg. 1.1015-4(a)(2)).

This generally gives us the following formula for determining the gift tax attributable to the net amount of appreciation (assuming one gifted property for the sake of simplicity):

The product of this formula (or formulas, for multiple gifts) gives us the amount by which basis will be increased. However, the basis increase cannot exceed the gift tax actually paid. Note also that if both gift and GST taxes are paid, this formula is iterated a second time in the same manner for GST tax (after adjustments for gift tax under IRC Section 1015). The GST tax increase to basis is a subject for another article.

Before moving on, note also that any tax imposed on a distribution from a QDOT to the beneficiary spouse is treated as a gift tax for purposes of this basis increase.

This basis increase for the gift tax attributable to net appreciation is treated as a basis increase under IRC Section 1016(a). See IRC Section 1015(d)(4), Treas. Reg. 1.1015-5(d), and Treas. Reg. 1.1016-5(p). While the GST tax basis adjustment is not directly addressed in these provisions, presumably it would also be treated as a basis adjustment under IRC Section 1016. The significance of this treatment is that, under IRC Section 1016(b), the basis increase for gift or GST taxes paid is deemed to occur after any adjustments to basis in the hands of the donor for the year of disposition.

These results, along with the treatment of basis in a part gift, part sale, could have additional wrinkles where a net gift is made. A net gift is generally a situation where the donee pays the gift tax, instead of the donor. While net gifts have not been as popular given the high gift tax lifetime basic exclusion, this is still a strategy that warrants a look in a separate article.

Note, however, that this rule would not apply where there is a gift of loss property (i.e., property where the donor’s basis is greater than the fair market value of the property) because the increase in basis requires there to be net appreciation at the time of the gift to begin with.

Conclusion

Basis is a concept often taken for granted in gifting. However, as seen above, we cannot assume a carryover basis in all situations. Likewise, we cannot assume a cost basis in all situations. Recognizing the situations in which basis is adjusted up or down – including for gifts – is a necessary prerequisite to informed tax planning. As we move into 2025, comparisons of these outcomes from both an income tax perspective and a transfer tax perspective will take on added importance.

And, while these general basis rules seem limited, the types of transfers can have downstream effects. In subsequent articles, we will examine issues such as the unified basis rule, net gifts, basis in grantor trusts and various installment and private annuity transactions, split interests, and depreciation schedules (including when a donee is deemed to place property in service for purposes thereof).