The Added “Work” of Crummey Power Accounting

Examining the accounting and management costs of withdrawal rights

Table of Contents

Accounting Issue Number 1: Other Annual Gifts and Crummey Powers

Accounting Issue Number 2: Growth of Lapsed and Unlapsed Portions

Accounting Issue Number 3: Tracking Use of Contributed Funds

Background

In several prior articles, we have examined the nuances of “Crummey” powers – a colloquial term given to rights of withdrawal in an irrevocable trust, which are used to create a present interest for a transfer in trust sufficient to qualify for the gift tax annual exclusion – and some of the issues inherent in these powers. These issues include but are not limited to the question of whether written notifications are required, the tax effects of the lapse of a Crummey powers, whether and how these powers get reported on a gift tax return, and effects of generation-skipping transfer (GST) tax on these powers.

Confusion reigns supreme in how to create, and administer, irrevocable trusts with Crummey powers. Many trustees are family members or friends of the settlor, and these trustees often lack guidance as to how exactly Crummey powers should be dealt with. Even in the professional ranks, finding attorneys, CPAs, wealth advisors, and fiduciaries who can adequately navigate Crummey powers can be a tall order, not to mention the lack of guidance a trust settlor’s advisors might be obligated to provide to a trustee. While there is a ton of attention on the notice requirements for Crummey powers and associated (possibly widespread) lack of compliance, these notice requirements are but a small sliver of the broader implications of Crummey powers.

The complications of Crummey powers, as we will discuss below, may not be worth it depending on the type of trust and broader gifting plan. For some trusts, like irrevocable life insurance trusts, the need to fund these trusts with annual premium payments creates a compelling reason to create Crummey withdrawal rights. But for other trusts – especially where one simply wishes to leverage annual exclusion gifts across multiple beneficiaries, on an annual basis – direct gifts may have advantages that are often lost in the broader scheme of what has come to be accepted as “prudent” planning. This is especially complicated, as we will see, in situations where transfers to trusts use both the settlor’s annual exclusions ($19,000 per donee in 2025) and lifetime gift tax applicable exclusion ($13,990,000 in 2025, plus any deceased spousal unused exclusion).

These complications are made worse by the lack of standardization. No two trusts granting Crummey powers are alike. If one reviews trusts drafted by other attorneys or firms, the reviewer often observes a miasma of blindly-cobbled trust provisions creating and addressing withdrawal rights. There are many different types of Crummey powers, which often vary based on how a lapse of the power is treated.

The following is a quick recap of some of the issues with Crummey powers, but if you would like to skip ahead click here.

Recap on Lapse

To recap, what do we mean by a “lapse” of a Crummey power? The power itself involves a window of time under which a beneficiary can withdraw (usually) their proportionate share of contributions to a trust during a given calendar year, up to the gift tax annual exclusion available to the donor (with respect to that beneficiary) at the time of the trust contribution.[1] Often, the intent is that this power not actually be exercised. So, to achieve some level of certainty for the trust, the withdrawal right is not perpetual in nature. Instead, it is given a limited shelf life – often 30 to 60 days, at the top of the bell curve – during which a beneficiary can exercise the power.

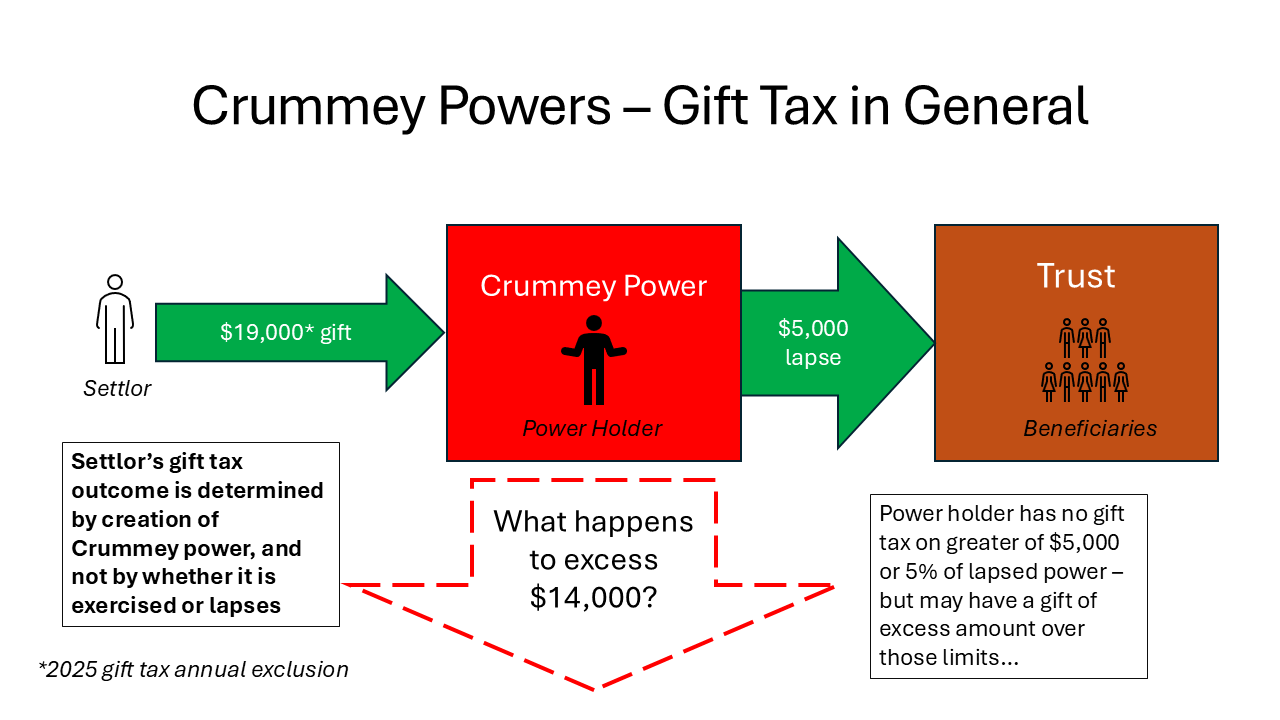

At the end of this time period, the power goes away (at least in part). The problem, however, arises in exactly how much of the power goes away. As discussed in prior articles, the power “going away” is treated as an event of gift tax significance through which the power holder (not the donor) is treated as making an indirect gift to the other trust beneficiaries. How much is this gift? It is hard to say, because some of the property subject to the Crummey power will still stay in trust for the power holder’s personal benefit. Yet, under principles of IRC Section 2702, this personal benefit is usually assigned a zero value because of the lack of certainty as to when, and how much, of the property subject to the power might benefit the power holder post-lapse. Our only certainty comes in the form of IRC Section 2514(e), which provides that there is no gift (from the power holder to the other trust beneficiaries) on the first $5,000 of the power that goes away in any calendar year.

This $5,000 limit is like the annual exclusion, in that it is a benefit that is refreshed every year. But unlike the annual exclusion – which applies per donee – this $5,000 limit is personal to just the power holder and cannot be multiplied or carried over if unused. This $5,000 limit is only part of the equation, however. Technically, this floor for gift treatment (when such a power goes away) is the greater of $5,000, or 5%. But, the 5% limit is often misapplied. This 5% limit only applies to the amount of cash or property that could be withdrawn under the power of appointment itself, and not to the value of the entire trust. Why? Because the limit applies to a lapse of a presently-exercisable general power of appointment, and the power holder’s power only applies to current-year (and sometimes carried over, unlapsed prior years’) trust contributions.

This creates an awkward mismatch between the annual exclusion available to the settlor, and the lapse exclusion available to the power holder.

Before moving on, you might be asking why the power holder does not themselves get an annual exclusion for this indirect gift to the other trust beneficiaries when their power goes away. The answer lies in the purpose of the Crummey right to begin with. The gift tax annual exclusion is not available for gifts of future interests. Most transfers in trust are gifts of future interests, because beneficiaries do not have the immediate, unrestricted right to the possession or enjoyment of property placed in trust – instead, they have to wait until a trustee grants this possession or enjoyment. Crummey rights create a way to manufacture immediate, unrestricted possession or enjoyment for trust contributions, thus qualifying the donor (settlor) for annual exclusion(s). But, when a Crummey power goes away, the property then passes to a trustee who controls possession or enjoyment moving forward. The outcome is that the power holder’s indirect gift is a gift of a future interest that does not qualify for the gift tax annual exclusion with respect to the power holder.

Circling back to the mismatch, this means a settlor (in 2025) can create Crummey powers of up to $19,000 per power holder in the trust. (Typically the IRS takes umbrage to a situation where the power holders are not otherwise beneficiaries of the trust, but that is a subject for another time and is an outcome for which the IRS has a losing record). But, the power can only go away $5,000 at a time[2] without creating gift and GST tax uncertainty for the power holders. This leaves an excess amount of $14,000. If the settlor and their spouse make joint or split gifts, this excess amount increases to as much as $33,000 ($19,000 x 2, minus $5,000).

How this excess $14,000 (or $33,000) is treated determines what type of Crummey power we have. It also dictates the GST tax effects of the entire $19,000 (or $38,000) Crummey power. Typically, these are our options for the excess amount, each of which is designed to keep the power holder from making a taxable gift to the other trust beneficiaries:

Hanging powers: Let the excess $14,000 carry over into the next year with a continuing right of withdrawal, where subsequent years’ $5,000/5% lapses can be applied.

Incomplete gift powers: Give the power holder a testamentary (limited or general) power of appointment over the excess $14,000, so that there is no completed gift to the other trust beneficiaries.

2642(c) powers: Hold the excess amount in a separate share trust for the sole lifetime benefit of the power holder, that will be included in their gross estate at death (but which qualifies for the GST tax annual exclusion) – this is often accompanied by a testamentary power of appointment such that incomplete gift treatment also applies.

2514(e) powers: Only allow the beneficiary to withdraw up to $5,000 instead of $19,000, so that there is no excess amount (and no GST tax ETIP issue with respect to a spouse who is given a Crummey power).

In each case, the $5,000 lapsed portion will be added to the general pool of trust assets from which each trust beneficiary (including the power holder, usually) can benefit – which under IRC Section 2514(e) should not result in a taxable gift from the power holder. And, for hanging powers (and correctly structured 2642(c) powers under which a power holder has a testamentary general power of appointment), subsequent years’ $5,000 lapses can apply to the carried over portion (assuming no other Crummey powers are created in that year, whether under the same trust or other trusts). For all but 2642(c) powers (or their equivalent structure for non-skip person power holders), however, maintaining full GST exemption requires allocation of the settlor’s GST exemption (and spouse’s GST exemption in a joint or split gift) to the entire $19,000 or $38,000 Crummey power – possibly requiring the filing of a gift tax return where automatic allocation does not apply.

Which brings us to the broader subject of today’s discussion – accounting for Crummey powers by the trustee.

Accounting Issue Number 1: Other Annual Gifts and Crummey Powers

Keep reading with a 7-day free trial

Subscribe to State of Estates to keep reading this post and get 7 days of free access to the full post archives.