Grantor Trusts: An Intro

Introducing a new series on income tax rules that are often misunderstood

Series Index

Table of Contents

Video Summary

Background

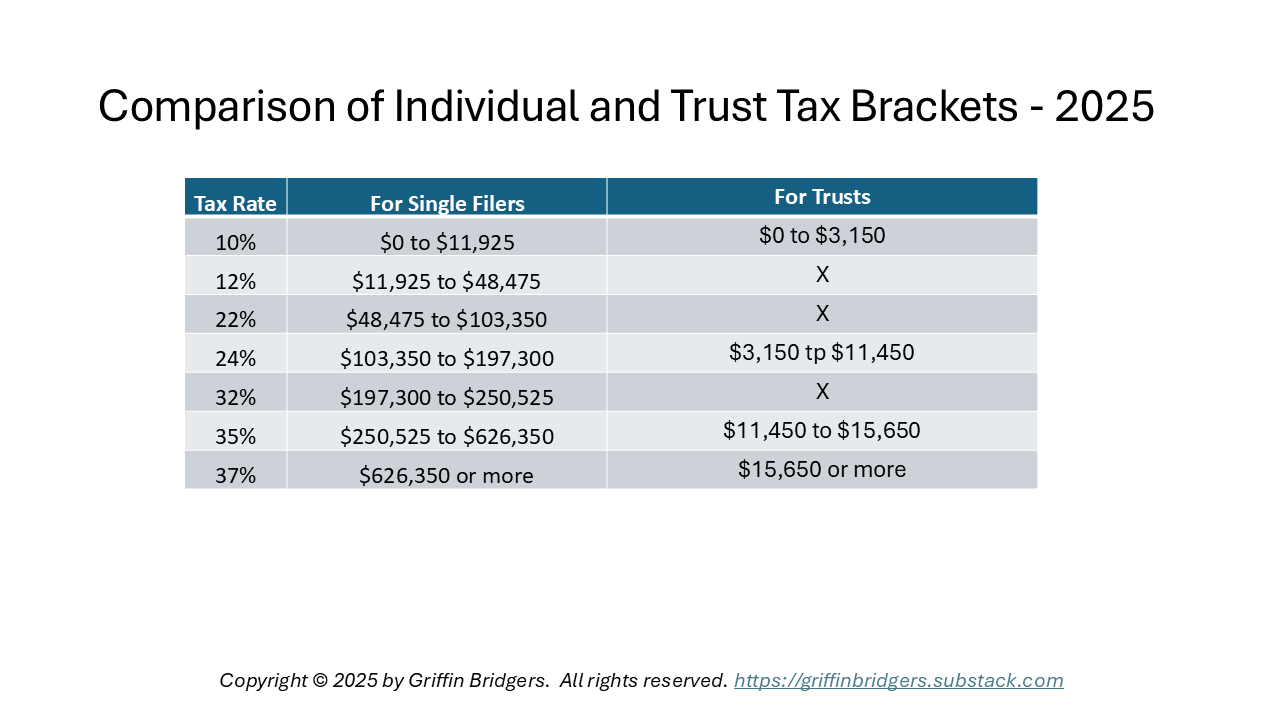

Trusts are generally recognized as separate, independent taxpayers for federal income tax purposes. Under Internal Revenue Code 1(e), trusts have their own income tax brackets that top out at the (current) highest individual income tax rate of 37%. But, these brackets are fewer, smaller, and more compressed than individual tax brackets as seen here:

But, this was not always the case. As recently as 1986, the brackets for individuals were significantly the same as for trusts. It wasn’t until the Internal Revenue Code of 1986 that the concept of compressed tax brackets became into being. Starting in 1987, we first saw the split between the brackets for individuals versus the brackets for trusts.

Under the income tax rules applicable to trusts, there is always an option to “shift” the taxation of (at least the accounting) income of the trust to individual beneficiaries by making a distribution during a calendar year, or (by election) within 65 days of the end of the calendar year. This gives the trust a distribution for what’s known as its “distributable net income,” or DNI, under IRC Sections 661 for simple trusts and 662 for complex trusts. Trusts still get the benefit of capital gains rates under IRC Section 1(h), but again the more compressed brackets mean that opportunities to use lower brackets on capital gains will be more limited when compared to individuals. And, while trustees may distribute net capital gains to beneficiaries, such gains are usually taxed to trust (and not eligible for the trust-level DNI deduction) unless the trustee is permitted to allocate capital gains to income under fairly-stringent rules combining federal tax law, state law applicable to fiduciary accounting, and the terms of the trust itself.

These complex rules, however, are not the focus of this article or series. Instead, before we can even apply these rules and brackets, we must determine whether certain rules set forth in IRC Sections 671-679 apply. These rules are commonly known as the “grantor trust” rules. They find their origin in the Internal Revenue Code of 1954.

Without belaboring the finer points of the history or origin of the grantor trust rules, such history being simplified in a conclusory manner here, the general intent of such rules was to limit opportunities for individuals to shift individual income to trusts over which substantial control was retained. Especially in the days of identical tax brackets for individuals and trusts, in theory, one could divide income between themselves and a trust in a way that lowers effective tax by riding up the brackets twice. The grantor trust rules were designed to prevent that outcome, depending on the degree of control retained over a trust, by “ignoring” the existence of such trusts for income tax purposes only.

Grantor Trust: A trust for which some or all taxable income, or corpus, is deemed to be owned by a grantor or beneficiary for income tax purposes only.

However, the 1986 changes ironically flipped these motivations in application. Arguably, the compression of the trust tax brackets continues to do more to discourage the shifting of at least ordinary income than the grantor trust rules themselves. Ironically, this has created an environment where, in many cases, the application of the grantor trust rules (to tax income to a grantor or deemed owner, individually) now creates lower effective income tax rates than if the trust itself was taxed on its income.

This brings us to current day, where grantor trusts are ubiquitous in estate planning and wealth transfers – especially for inter vivos trusts (i.e., those created during the life of a grantor). In this series of articles, we will explore some of the basics you need to know about the grantor trust rules and their application.

Deemed Ownership

The backbone of the grantor trust rules is deemed income tax ownership. In other words, ignoring the existence of the trust for income tax purposes is not enough. We must determine someone else with a relationship to the trust – usually an individual grantor, donor, or beneficiary - who will instead be taxed on income generated by assets generated to the trust.

In many cases, this deemed owner will be the grantor of the trust. In determining the identity of the grantor of the trust, we start with each individual signing off on the creation of the trust in any of the synonymous capacities of grantor, settlor, trustor, trustmaker, donor, etc. But, there can be no income of the trust to be assigned to a deemed owner unless there are assets inside said trust. And, if someone other than the grantor puts assets into the trust, shifting the income on those assets to the grantor themselves (i.e., between individuals through a trust instead of between an individual and a trust itself) would seem to violate the goal of discouraging the shifting of income to begin with.

So, under Treas. Reg. 1.671-2(e), a “grantor” is defined to include anyone who makes a “gratuitous transfer” to a trust. While the definition is much more nuanced, Reg. 1.671-2(e)(2) generally defines a gratuitous transfer as a transfer for less than fair market value. But, this does not depend on whether a gift is actually made to the trust for gift tax purposes. As we will explore below, gratuitous transfers are generally only those transfers made during the life of a grantor.

To avoid income shifting between individuals through the trust, income of the trust that is deemed to be owned by a grantor for income tax purposes will be traced to the assets gratuitously transferred by that grantor. But, in order for that to occur, the grantor must retain certain rights or powers over those gratuitously-transferred assets. Those rights, which are generally covered in IRC Sections 671-677, will be the subject of subsequent articles.

There is a Code Section, however – IRC Section 678 – which in certain cases treats a beneficiary, instead of the grantor, as the deemed owner of trust assets. This determination is not based on the beneficiary’s gratuitous transfers, but instead on the beneficiary’s current or previously-released powers to withdraw income and/or corpus (principal) of the trust. These rules find their origin in the 9th Circuit’s holding in Mallinckrodt v. Nunan, 146 F.2d 1 (1945). In Mallinckrodt, the 9th Circuit affirmed the Tax Court’s determination that a beneficiary’s unrestricted right to withdraw trust income meant that the beneficiary (instead of the trust) should be taxed on that income regardless of whether the income was actually withdrawn, or instead accumulated in the trust and added to corpus.

Code Section 678 will be covered in greater detail in subsequent articles, but for now it has an even more important function to note – an ordering rule. After all, what if a beneficiary and grantor are treated as the deemed income tax owners of the same assets? To resolve this potential conflict, IRC Section 678(b) provides:

Subsection (a) [deeming a beneficiary as income tax owner] shall not apply with respect to a power over income, as originally granted or thereafter modified, if the grantor of the trust or a transferor (to whom section 679 applies) is otherwise treated as the owner under the provisions of this subpart other than this section.

More simply put, this means the grantor always wins out if the grantor and beneficiary are deemed income tax owners of the same trust assets or income (or portion thereof).

Along these lines, it is important to note that deemed income tax owner does not always apply to the entire trust, or a grantor’s entire transfer. It extends only so far as certain powers, and other rules, dictate. So, it may be the case that the grantor or a beneficiary is the deemed income tax owner of only a portion of trust income, or trust corpus. When it comes to tax ownership of tax corpus, it may also be the case that capital gains (that traditionally are assigned to corpus under trust accounting rules) are taxed to a deemed owner while other income generated by that corpus is not. We will explore some of these permutations throughout this article series.

Likewise, the grantor trust rules only apply for income tax purposes. They do not create deemed ownership for estate or gift tax purposes. While there have been proposals to remove this bifurcation of income tax and transfer tax treatment, no such proposals have passed. However, some powers that create deemed income tax ownership for a grantor or beneficiary may have crossover with certain retained interests, powers of appointment, etc. that can create deemed transfer tax ownership. These crossovers will be explored in this series as well, usually on a power-by-power basis – leaving us with a set of commonly-accepted grantor trust powers that should not create, when properly structured and administered, an incomplete gift or gross estate inclusion. But, this leaves us with a broader question of what happens when someone dies holding a grantor trust power?

Types of Trusts to which the Grantor Trust Rules Apply

Generally, the grantor trust rules can only apply to a deemed owner who is actually living or in existence. While, under Treas. Reg. 1.671-2(e)(4), a partnership or corporation is acknowledged as a potential grantor by virtue of a gratuitous transfer, most estate planning situations involve individuals as deemed owners. This means the death of an individual deemed owner terminates grantor trust status, at least with respect to the portion of the trust to which that decedent’s deemed ownership extends. This itself might create a deemed income tax transfer from decedent to the trust, but this deemed transfer itself generally will not lead to a step-up in tax basis at least in the eyes of the IRS.

This means testamentary trusts (i.e., trusts created under a will) cannot be grantor trusts with respect to the deceased grantor. They can, however, be grantor trusts with respect to a beneficiary – but only under the rules of IRC Section 678 (which, as we will later explore, may also invoke and attribute definitions and powers traditionally examined with respect to just the grantor under IRC Sections 671-677). And, it may be the case that the death of the grantor invokes the ordering rule of IRC Section 678(b) to create a deemed income tax transfer of ownership from grantor to beneficiary, instead.

Most cases involving grantor trusts, therefore, will apply to inter vivos trusts – i.e., trusts created during the life of the grantor. Inver vivos trusts can be revocable or irrevocable. This distinction is not expressly made under the grantor trust rules, which instead apply to any trust. But, the right to revoke itself is treated as a right that invokes the grantor trust rules under IRC Section 676. For this reason, revocable trusts will practically always be grantor trusts. So, application of the grantor trust rules will have primary relevance for inter vivos irrevocable trusts. It is possible, however, that a right to revoke may only apply to a portion of a trust – usually consisting of a grantor's gratuitous transfers to that trust. This might be seen, for example, in a joint revocable trust.

All In? Exploring Rev. Rul. 85-13

In many cases, the benefits of grantor trust status are best leveraged where deemed ownership of all trust corpus and income extends to a grantor or beneficiary. But, this 100% outcome cannot be assumed. When examining a trust to determine grantor trust status, one must be conscious of the possibility that the trust itself may still be taxed on some income. This also means distinguishing between taxable income of a trust, which is a creature of federal tax law, and trust accounting income, which is a creature of state law.

But, when we circle back to the gratuitous transfer rules above, recall that their only utility is to classify a transferor of property to the trust as a grantor to begin with. The level of “gratuitousness” does not itself affect the broader determination of what portion of that contributed property is subject to deemed ownership under the grantor trust rules. Instead, we must be concerned with what powers are retained by the grantor after the gratuitous transfer. And, keep in mind that these powers may also have relevance to property (or income relating thereto) actually owned by the grantor, or the trust, immediately before a transaction.

So, for example, if the grantor sold property at a discount to the trust (i.e., for less than fair market value), only the bargain portion would be a true “gratuitous” transfer. But, if the grantor retained certain powers over all of the transferred property after the transfer under IRC Sections 671-677, then the grantor would be treated as the deemed owner of all of that transferred property. This would be a boon if, for example, this deemed ownership of the sold property both before and after the discount sale kept the grantor from recognizing gain by, in essence, “selling to themselves” as deemed owner.

It is this very principle around which Rev. Rul. 85-13 is based. This Ruling is often cited for the proposition that transactions between a grantor and a grantor trust cannot be treated as taxable sales or exchanges for federal income tax purposes, even though the grantor trust rules only affect the taxation of trust income (and not income of the grantor themselves resulting from transactions with a grantor trust). But, the facts of this Ruling applied to a trust for which the grantor was the deemed owner of the entire trust. While we will discuss this Ruling in a separate articles and cite it throughout this series, an important take-away is that the deemed ownership of the property subject to a sale or exchange by a grantor must have a certain unity of actual or deemed ownership between grantor and trust both before and after the sale or exchange.

But, this deemed ownership may not always be asset-specific when considering the assets given up in an exchange, versus the consideration received. As discussed in the following video on Private Letter Ruling 202022002, it is possible that a power that only extends to consideration received (and not to the assets being sold) may still be enough to prevent a sale from being taxable under Rev. Rul. 85-13. It is also possible that a grantor can be the deemed owner of multiple trusts, in transaction where it might otherwise appear that one trust is the deemed owner of the other under the grantor trust rules:

What’s Next?

As we go through this series, this root article will contain a series index at the top as with other series in this newsletter. This will allow you to navigate to this root article to see subsequent installments as they come out. Videos such as the one at the top will be included, but (as noted below) sometimes after a paywall.

Note also that this series will not address every nuance of grantor trusts. These rules have a long, storied history and they have been examined in several cases and rulings. The learning objective of this series is not to become a black belt in grantor trusts, but instead to perhaps become a blue, brown, or red belt.[1]

And, the complexity of the material will vary. In some cases, Code provisions and Treasury Regulations will provide seemingly-straightforward answers. In other cases, there will be highly nuanced examinations of trusts, cases, rulings, and fact patterns. For an example of what might be an article with higher complexity in this series, see this discussion of certain grantor trust rules relating to ILITs.

Finally, while some articles in this series will be fully available to the reading public, the nature of this material necessitates that some articles or portions thereof will only be for paid subscribers. But, each paid article will have a free preview that still has valuable education. And, while I never recommend using recommended language sight unseen without edits or understanding, I will aim to provide some sample language (also behind a paywall) throughout this series.

[1] Based on common belts used in Tae Kwon Do, of which the author has familiarity, and not necessarily other martial arts.