Grantor Trusts and Voting Rights

Exploring IRC Section 675(4)(A)

Table of Contents

Background

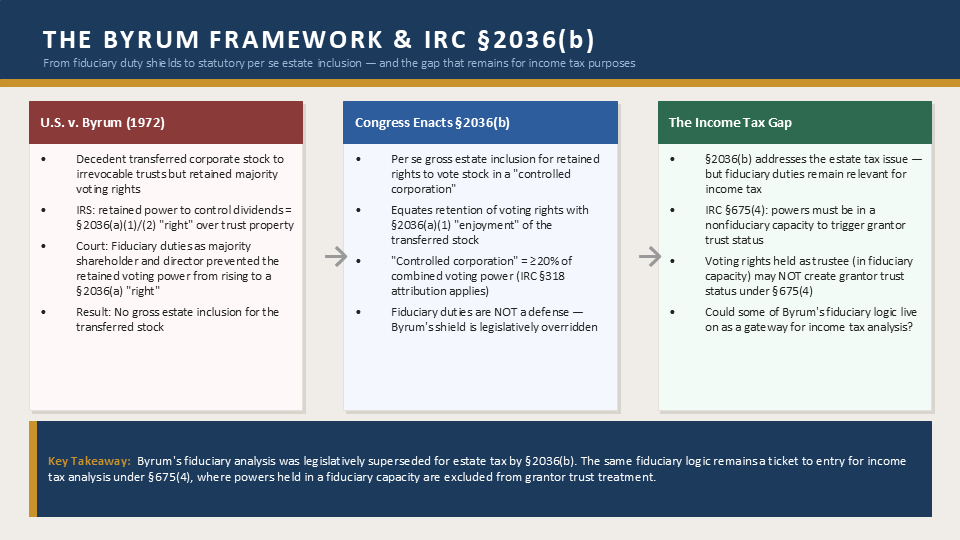

The retention of voting rights over stock transferred during life has a storied history. A long-standing U.S. Supreme Court opinion in U.S. v. Byrum, 408 U.S. 125 (1972), serves as one of the cornerstone authorities for analyzing the estate tax effects of lifetime transfers of corporate stock. In this case, during his life the decedent had transferred stock to three irrevocable trusts for the benefit of his children with a bank as trustee. However, he had retained the right to vote the corporate stock which, in conjunction with his individually-owned shares of stock gave him the majority vote.

The Service argued that the retention of the right to vote the shares of stock in the trusts was tantamount to a power to control income from the corporation to the trust, as (1) the decedent had the right by virtue of the majority of voting power to elect directors, (2) the directors, in turn, controlled dividend policy, and (3) this in essence gave the decedent the power to determine if and when dividends were declared with respect to the trust. Taken together, this would mean the decedent maintained control over the transferred stock under IRC Section 2036(a)(2), and/or possession and enjoyment over the stock under IRC Section 2036(a)(1). The Court, however, determined that business concerns as well as the relevant fiduciary duties of both a majority shareholder and a corporate director would prevent the decedent’s de facto powers (in the form of voting rights) from rising to the level of a “right” described in IRC Section 2036(a).

Later, as a result of this case, Congress enacted IRC Section 2036(b) to create gross estate inclusion per se for any directly or indirectly retained rights to vote stock in a “controlled corporation.” This Code Section equates the retention of voting rights with the retention of the “enjoyment” of the corporate stock under IRC Section 2036(a)(1). For this purpose, a “controlled corporation” is one in which the decedent has retained at least 20% of the combined voting power of a corporation. At first blush it may appear that this is intended to describe a corporation for state law purposes, but IRC Section 2036(b)(2) adds that IRC Section 318’s attribution rule (applicable to any entity taxed as a C or S corporation) applies in determining whether this 20% threshold is satisfied.

Subsequent analyses with respect to family limited partnerships have similarly disregarded fiduciary duties as a panacea to the application of IRC Section 2036(a). These duties are a subject for another time, but the presence or absence of fiduciary duties can still have vital implications for income tax purposes with regard to voting and investment rights under the grantor trust rules. This article explores some of these implications.

Voting Rights and IRC Section 675(4)(A)

Previously, we covered IRC Section 675(4)(C) as a grantor trust power. This power permits a grantor, in a nonfiduciary capacity, to substitute their own assets for trust assets having “equivalent value.” And because of IRC Section 2036(b), such a power often excludes voting stock (held by the trust) in order to prevent an inadvertent attribution of voting power to the grantor. This could actually be a boon if, for example, a trust holds QSBS that is voting stock where a goal of the trust is non-grantor status with respect to such QSBS (in order for the trust to potentially avail itself of a separate QSBS gain exclusion as a separate taxpayer under IRC Section 1202(b)).