Family Limited Partnerships and IRC Section 2036: A High-Level Overview

Useful planning tips at the intersection of business principles and gifting principles

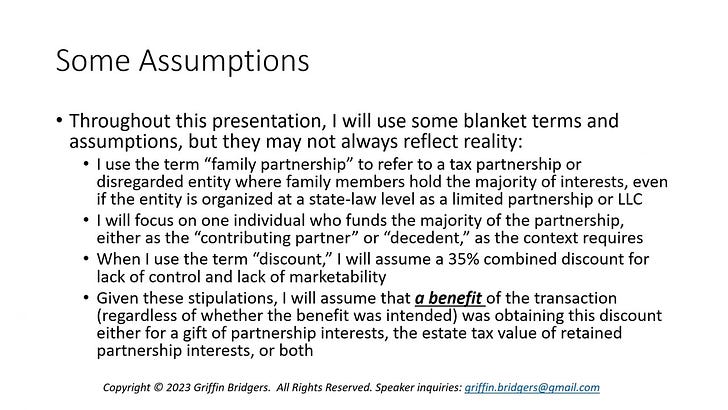

Intro and Caveats

One of my goals in this newsletter is to make complex concepts digestible for practitioners like you. This newsletter is not designed to be a U.S. Tax Court brief or law review article, and for the most part my fellow practitioners respect that. But, one of the most controversial topics I have attempted to tackle is the issue of family limited partnerships, and even the higher-level intersection of IRC Section 2036 with business principles. This is an area where the academics and technicians love to play, shine, and (dare I say) show off. It is also the area where I have received the most criticism, some warranted but some for my intrusion into fiefdoms.

A year ago, I had a course ready for launch on this very issue. Regrettably, I let myself get intimidated by the academics and aforesaid criticism and in the process lost sight of two important personal principles: (1) making my content actionable, and (2) creating a framework for younger practitioners to not get intimidated by the academics and critics in their respective industries.

So, a year delayed, I am picking up the mantle on this overdue course. It is not complete, and I’m sure any ACTEC fellow or experienced practitioner can find ways to pick it apart. It does not do justice to the whole “fiduciary duty under IRC Section 2036(a)(2)” debate. It does not perfectly cite (in Bluebook format) the myriad cases in this area, nor does it cover all relevant cases in this area. It does not fully address the intersection of the donut hole issue and double-taxation of assets under IRC Section 2043 from Powell. My analyses and conclusions are too simple in some cases. Instead, depth has on occasion been triaged in favor of creating a useful course.

What this course does succeed at is extracting some high-level principles that are often crowded out by the academic debates, along with some principles that may fly under the radar, to better equip wealth transfer professionals to analyze some of the common issues inherent where IRC Section 2036 interacts with business entities, most often family limited partnerships.

Below I have embedded course slides, and the video for this course. The video is ~2.5 hours in length.

Course Slides

Video

Conclusion

If you enjoyed this, please stay tuned - I have courses similar to this coming down the pike, but with a breakdown of videos into 10-minute segments. Something similar can be seen in this course on the Corporate Transparency Act. In the queue is a comprehensive course on the grantor trust rules, along with a refinement of my content on generation-skipping transfer tax. For more of this type of content, please consider a paid subscription.